WoV stock portfolio

Quote: billryanOut of curiosity, why invest in bonds? I've always looked at bonds as a means to preserve money, not to grow it. If you are a long way from retiring, why tie up money in a long term low interest investment?

a) I'm a conservative investor.

b) I use bonds as my emergency fund.

Quote: billryanOut of curiosity, why invest in bonds? I've always looked at bonds as a means to preserve money, not to grow it. If you are a long way from retiring, why tie up money in a long term low interest investment?

Agree. I had no bonds for the first 20 or so years of investing. As I neared retirement I started shifting some to bonds. My first 20 years I outperformed my peers who had 'advisors' keep them in 50% stocks, 40% bonds, 10% cash or whatever silly formula they used. If your horizon is greater than 10 years I think stock is the way to go.

But now with the market meltdown, the fed might lower interest rates which will make my bonds worth more.

I'm in a Catch 22?

well that was quick... the Fed just cut rates by .5%.Quote: 100xOddsI was going to switch bonds back to stock when that portfolio is+15% more than the theo stock portfolio.

But now with the market meltdown, the fed might lower interest rates which will make my bonds worth more.

I'm in a Catch 22?

lets see how high my bonds jump.

edit:

and soon after the surprise rate cut, the market turns negative.

When the FED cuts interest rates, the price of risky Zero Coupon Bonds goes up.

They also rise dramatically when stocks prices fall.

ZROZ is up 20% since the start of the year.

how are zero bonds different that vanguard's total bond fund or their long corp bonds? (My portfolio is 25% and 25% in them )Quote: TankoWhen the FED cuts interest rates, the price of risky Zero Coupon Bonds goes up.

They also rise dramatically when stocks prices fall.

ZROZ is up 20% since the start of the year.

Quote: 100xOddshow are zero bonds different that vanguard's total bond fund or their long corp bonds? (My portfolio is 25% and 25% in them )Quote: TankoWhen the FED cuts interest rates, the price of risky Zero Coupon Bonds goes up.

They also rise dramatically when stocks prices fall.

ZROZ is up 20% since the start of the year.

No real difference. The moment you buy a bond or bond fund you are presumably getting a fair price at the present day's interest rates. If you sell the bonds when interest rates are higher you will get less than you paid. If you sell them when interest rates are lower you will get more than you paid.

For the majority of us 'regular Joes' we buy a bond or CD and are just expecting to get the agreed upon interest rate for the term of the bond. Let's say I bought a $1000 bond last year that will pay me 3% interest for 5 years. I will get $30 a year for each of those 5 years then get my $1000 back. But if I look at my portfolio, it will list the bond as being worth $1050 or so now. But that's not how I use it. To me it still is the same $1000 in 5 years plus $30 a year.

Quote: 100xOddshow are zero bonds different that vanguard's total bond fund or their long corp bonds?

Those appear to be regular bond funds, with no Zeros.

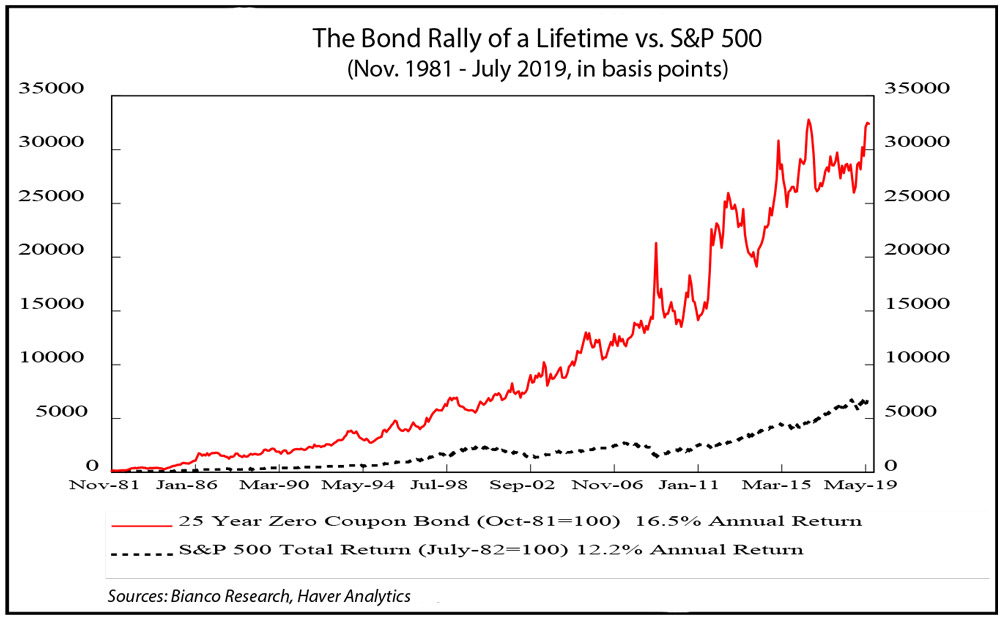

Unlike regular bonds, Zero�s do not pay interest, but are sold at a deep discount. The bond holder is paid upon maturity of the bond.

They are riskier because they are more sensitive to interest rate swings than regular bonds, but they have had excellent performance over the past 25 years.

Zero�s vs. S&P over the past 25 years.

ZROZ has more than doubled since 2009. Compare that to BND which was $75 in 1986 and $87 today. Good ETF's. So is AGG.

There is a time when bonds make sense, but I don't think it's now.

Others opinions and mileage will vary.

Quote: billryanWhen you buy a bond when rates are so low, you are pretty much eliminating any potential upside. If you need to sell you will almost certainly lose money. If you hold it to maturity, odds are inflation will eat away much of the earnings. Give them $1000, get $30 a year for five years and with just two percent inflation, the $1000 you receive back has $900 in today's buying power.

There is a time when bonds make sense, but I don't think it's now.

Others opinions and mileage will vary.

I agree with you. I think the 10 year Treasury Bond yield is around ONE PERCENT a year now! My 3% example doesn't exist now. No way you can get a non junk bond paying a mammoth 3% over 5 years now.

But many people thought that over the past year or two interest rates couldn't possibly go any lower (including me!) We were wrong, and it's why bonds and bond funds have done well over last two years.

I bought a small stake In Delta today..... because Warren Buffet said so.....

I guess I'm a dinosaur?Quote: TankoZero�s vs. S&P over the past 25 years.

ZROZ has more than doubled since 2009. Compare that to BND which was $75 in 1986 and $87 today. Good ETF's. So is AGG.

I follow vanguard's total intl 25%, total bonds 25%, total market 50%. (Then switched 25% of total market to long corp Bonds because I expected a crash 2 years ago.)

For bonds only increasing $12 in 11 years, that's just the nav? It doesn't include the interest?

You nailed it in one.Quote: 100xOdds

For bonds only increasing $12 in 11 years, that's just the nav? It doesn't include the interest?

not even the Fed's move stopped the swoon today

Quote: 100xOddsI guess I'm a dinosaur?Quote: TankoZero�s vs. S&P over the past 25 years.

ZROZ has more than doubled since 2009. Compare that to BND which was $75 in 1986 and $87 today. Good ETF's. So is AGG.

I follow vanguard's total intl 25%, total bonds 25%, total market 50%. (Then switched 25% of total market to long Bonds because I expected a crash 2 years ago.)

For bonds only increasing $12 in 11 years, that's just the nav? It doesn't include the interest?

Correct. Zero coupon bonds which you are discussing do not pay interest during the course of their lifetime. So there is nothing to 'include'. You pay, lets say $500, and ten years later it pays $1000.

Quote: SOOPOOI bought a small stake In Delta today..... because Warren Buffet said so.....

Strong company. He likes companies that have lots of levered free cash available.

He also bought KHC in 2013 and lost $5 billion when it hit a record low last year. It�s lower than that today.

2019 was Buffet�s worst year in a decade. Berkshshire was up 11%, while the S&P gained 29%.

saudi has declared an oil war with it's former partner, Russia.Quote: 100xOddsI was going to switch bonds back to stock when that portfolio is+15% more than the theo stock portfolio.

But now with the market meltdown, the fed might lower interest rates which will make my bonds worth more.

I'm in a Catch 22?

oil in a freefall and it's bringing down the s+p (-4%) in premarket.

it's expected the FED will lower interest rates.

That makes my corp long bonds worth more, right?

finally, after 2 years, Bab's financial advisor's advice paid off. :)

my current bond heavy portfolio is at least +20% over the theo portfolio of not switching.

now to wait for 3 straight days of gains to switch corp bonds back to stocks.

But the bond fund was still +20% more than if I didn't convert 25% of my stocks to it.

Now I have all this cash.

Waiting for 3 up days before buying stocks again.

Edit:

What do you all think about dollar cost averaging back into the market?

Ie: 1/3 of my cash into vti (total stock market fund) this week, 1/3 next week, and last 1/3 the week after that?

Quote: 100xOddsWith today's huge drop, I sold my corp bond fund because Yields were rising. That was dropping the value of the fund -8% total these past 2 days.

But the bond fund was still +20% more than if I didn't convert 25% of my stocks to it.

Now I have all this cash.

Waiting for 3 up days before buying stocks again.

Edit:

What do you all think about dollar cost averaging back into the market?

Ie: 1/3 of my cash into vti (total stock market fund) this week, 1/3 next week, and last 1/3 the week after that?

I wish I was as cautious as you were. I was around 30% in bonds but now I've sold a bit and am basically 50% bonds, 50% stocks. That's mostly of course because of the precipitous drop in stock value. WoV portfolio is still up 35% from inception, but down 20%+ from its peak.

Someone up thread mentioned IF the market starts coming back it will not be nearly as quickly as it fell. So a dollar cost averaging approach will make sense. But what makes you think the market won't continue its decline over the next 3 weeks? I guess if you put your caveat that you are waiting for 3 straight days up I like your plan.

Here is a table showing stock prices of some gaming companies on 1/1/20 and today (3/12/30):

| Company | 1-1-20 | 3-12-20 | Drop |

|---|---|---|---|

| Sands | 69.88 | 44.15 | 36.8% |

| MGM | 33.66 | 15.26 | 54.7% |

| Wynn | 143.6 | 68.02 | 52.6% |

| Caesars | 13.6 | 7.89 | 42.0% |

| Boyd | 30.05 | 14.54 | 51.6% |

| S&P 500 | 3244.67 | 2480.64 | 23.5% |

As you can see, gaming companies, in general, have taken a beating much more than the S&P average. I sold a rental house about six months ago and am still sitting on the cash. In other posts, I've estimated US Coronavirus deaths to be about 3,000. Whenever we start to see a leveling off, as China is seeing now, I plan to buy something. Probably casino stocks, given the huge hit they've taken, but I'm not sure. There is no rational reason these stocks should have fallen this much over something that will kill as many people in the US as tobaccos does in two days.

yeah, i think i'll use waiting for 3 straight up days b4 implementing my dollar cost averaging.Quote: SOOPOOI wish I was as cautious as you were. I was around 30% in bonds but now I've sold a bit and am basically 50% bonds, 50% stocks. That's mostly of course because of the precipitous drop in stock value. WoV portfolio is still up 35% from inception, but down 20%+ from its peak.

Someone up thread mentioned IF the market starts coming back it will not be nearly as quickly as it fell. So a dollar cost averaging approach will make sense. But what makes you think the market won't continue its decline over the next 3 weeks? I guess if you put your caveat that you are waiting for 3 straight days up I like your plan.

near closing of the 3rd up day, i'll put 1/3 of my cash into the total stock fund.

then another 1/3 the following week, and the last 1/3 the week after that.

edit:

just so i dont forget, here's the closing prices on 3/12.

corp bonds $11.06

total market $60.69

Let's see how lucky I am with my gamble...

Quote: WizardThis is what I think is my first post in this thread.

Here is a table showing stock prices of some gaming companies on 1/1/20 and today (3/12/30):

FYI, Genting is down 36% ytd, but apparently their stock is kind of all over the place in general, so I don't know if that's saying much.

ah.. so you are dollar cost averaging 20% at a time so 5 block buys.Quote: WizardI just spent about 20% of my cash on hand on an S&P index fund. Plan to throw in the rest while the market is low in blocks at a time.

you have a signal of when to buy?

or just going to wing it and wild ass guess it?

is there a gambling etf?Quote: WizardThis is what I think is my first post in this thread.

Here is a table showing stock prices of some gaming companies on 1/1/20 and today (3/12/30):

Company 1-1-20 3-12-20 Drop Sands 69.88 44.15 36.8% MGM 33.66 15.26 54.7% Wynn 143.6 68.02 52.6% Caesars 13.6 7.89 42.0% Boyd 30.05 14.54 51.6% S&P 500 3244.67 2480.64 23.5%

As you can see, gaming companies, in general, have taken a beating much more than the S&P average. I sold a rental house about six months ago and am still sitting on the cash. In other posts, I've estimated US Coronavirus deaths to be about 3,000. Whenever we start to see a leveling off, as China is seeing now, I plan to buy something. Probably casino stocks, given the huge hit they've taken, but I'm not sure. There is no rational reason these stocks should have fallen this much over something that will kill as many people in the US as tobaccos does in two days.

if not, i guess you can buy consumer discretionary etf.

Quote: 100xOddsis there a gambling etf?

Yes, you want BJK, VanEck. Trading at $28 right now.

I sold some stocks when the market was at it's peak in a taxed joint account that we shouldn't have to touch for quite a while- I really didn't want to sell them, but I just felt I should sell some. Now I am buying stocks at these lows in this particular account and am gambling I can get even better bargains next week - but I have mostly bought it all back in that account now, that had priority as I want it to be all stocks.

In retirement accounts, which were plenty heavy in bonds, I have sold quite a bit of the bonds to get the capital gains and plan to buy them back for the most part when 10 yr benchmark interest rates get at least closer to 2%, like 1.7% or so. I have confidence that rates will get back to that btw, but I admit it is another gamble. I also have bought some stocks with that money. I did hear somebody on CNBC say you might as well sell all your bonds to take gains , maybe just put it in SIPC guaranteed money funds that will pay close to zip but won't depreciate. I honestly don't know if 'to sell all bonds' is good advice or not, and so I haven't done that.

If stocks keep going down any further I will buy them in blocks, dollar cost averaging, in the retirement accounts as well, in fact that started when the stock market hit its recent low. Around 30% off recent highs is what I'm really looking for, then I will be buying, and if stocks go down more I will still be buying. If stocks stop going down I will put the money back into bond funds when the price is right.

I went with a similar dollar cost averaging plan in 2009 and it really paid off for me bigtime. I wish everybody luck!

when do you buy? what's the signal you use?Quote: odiousgambitI have been buying stocks on a dollar cost averaging basis too, my plan is a little different

I sold some stocks when the market was at it's peak in a taxed joint account that we shouldn't have to touch for quite a while- I really didn't want to sell them, but I just felt I should sell some. Now I am buying stocks at these lows in this particular account and am gambling I can get even better bargains next week - but I have mostly bought it all back in that account now, that had priority as I want it to be all stocks.

In retirement accounts, which were plenty heavy in bonds, I have sold quite a bit of the bonds to get the capital gains and plan to buy them back for the most part when 10 yr benchmark interest rates get at least closer to 2%, like 1.7% or so. I have confidence that rates will get back to that btw, but I admit it is another gamble. I also have bought some stocks with that money. I did hear somebody on CNBC say you might as well sell all your bonds to take gains , maybe just put it in SIPC guaranteed money funds that will pay close to zip but won't depreciate. I honestly don't know if 'to sell all bonds' is good advice or not, and so I haven't done that.

If stocks keep going down any further I will buy them in blocks, dollar cost averaging, in the retirement accounts as well, in fact that started when the stock market hit its recent low. Around 30% off recent highs is what I'm really looking for, then I will be buying, and if stocks go down more I will still be buying. If stocks stop going down I will put the money back into bond funds when the price is right.

I went with a similar dollar cost averaging plan in 2009 and it really paid off for me bigtime. I wish everybody luck!

every x% decline of the stock market?

every 2 weeks no matter how the market does?

and how many % of your available cash do you use for each buy?

also, i know nothing about Bonds.

i got lucky in picking Corp Bonds when i exchanged 25% of my portfolio to it.

i didnt want the same Total Bond Fund that my portfolio has because it would have made it harder to track.

(looking back, that is a REALLY dumb reason to pick a fund to put 6 figures into.)

Quote: WizardI just spent about 20% of my cash on hand on an S&P index fund. Plan to throw in the rest while the market is low in blocks at a time.

I'm planning the same thing, but the gambler in me is tempted to go into the leveraged ones since stocks are so low! What do you guys think of the TQQQ? Any ETF tracking S&P 500 that is even more leveraged? I'm young, don't have much cash savings atm but earning well so I can make it back if it goes poof..

I get prompted by lows that match lows in the past, currently the approx 22000 in the Dow exceeds a bit the low of Dec 2018. The replacement of what I reluctantly sold at the recent high took enough priority to have me dollar-cost-averaged down 25% of the generated cash each time roughly to this point. Now I am starting to buy stocks, if it keeps going down, for the retirement funds too with the bond money, a little arbitrarily looking for about 21250 Dow for the next step. If it doesn't happen I'll buy bonds at benchmark 1.75% or so in the 10 and dollar cost average that. Hope that isn't a long wait.Quote: 100xOddswhen do you buy? what's the signal you use?

every x% decline of the stock market?

every 2 weeks no matter how the market does?

and how many % of your available cash do you use for each buy?

Just use funds* like the vanguard fund BIV so you can see how the value goes up and down. The connection between increasing yield and lowering price and vice versa is not perfect correlation, so you don't buy or sell based on yield news alone [in spite of the simplistic strategy I indicated above] . This article is very good btw, https://paulmerriman.com/bonds-buy-sell-hold/Quote:also, i know nothing about Bonds.

*whatever you do don't buy any bonds at prices now!

the corp bonds i sold yesterday went DOWN -1% today?!

why didn't the corp bonds also go up?

the correlation is between the *rates* that the bonds pay and the price, not directly whether people are selling or buying stocks. Sure, usually when folks sell stocks they buy bonds, or vice versa, but this is not a perfect correlation. The correlation between rates and bond prices is also not perfect, especially in a bond fund.Quote: 100xOddsso the dow climbs 1900 points (+9%).

the corp bonds i sold yesterday went DOWN -1% today?!

why didn't the corp bonds also go up?

Your remark may mean that the rate went down 1%, not the price. If so it suggests investors then would have been buying bonds as well as stocks.

If you mean the price of the bonds went down, not the rate, investors have been selling bonds [net] and this is usually what goes on when stocks go up, but you can't count on it.

Benchmark rates are going up a bit, price down a bit, in the bond funds I own- this seems to be because rates were ridiculously low a few days ago and that could not be sustained

It has pros and cons, but I disagree that it deserves contempt like 'hit and run'Quote: OnceDearDollar Cost Averaging is of the same value as 'Hit and Run' It provides no EV advantage.

It has advocates within the better elements of the investment community since it is a strategy that avoids market timing and is usually the one used in employee's stock purchase plans

I will grant you the way I am doing it now involves market timing*, I'll listen to criticism

one of the bad things about rebalancing is that for most people it causes paralysis as they try to market-time. At the top of the market, they won't sell because "what if it goes up more?" and in times like these they won't buy because "what if stocks go down more?" . If you can tell yourself you accept these things and trust in dollar cost averaging, it helps get rid of that paralysis. YMMV

https://www.fool.com/investing/dollar-cost-averaging-what-investors-need-to-know.aspx

*an investor though avoids this criticism if he can point to rebalancing, which I am doing, and which gets the blessings of all the investment gurus.

Just like rebalancing, it has value as an hedging strategy. But, I still assert it adds nothing to EV. Like Martingale, it just changes the shape of the bankroll progress chart. If it did add to EV, we could just 'double dollar average' where we spend double each time the price drops ready for the huge benefit when it rises again..... if it rises again in our lifetime.Quote: odiousgambitIt has pros and cons, but I disagree that it deserves contempt like 'hit and run'

It has advocates within the better elements of the investment community since it is a strategy that avoids market timing and is usually the one used in employee's stock purchase plans ...

*an investor though avoids this criticism if he can point to rebalancing, which I am doing, and which gets the blessings of all the investment gurus.

Quote: OnceDearJust like rebalancing, it has value as an hedging strategy. But, I still assert it adds nothing to EV. Like Martingale, it just changes the shape of the bankroll progress chart. If it did add to EV, we could just 'double dollar average' where we spend double each time the price drops ready for the huge benefit when it rises again..... if it rises again in our lifetime.Quote: odiousgambitIt has pros and cons, but I disagree that it deserves contempt like 'hit and run'

It has advocates within the better elements of the investment community since it is a strategy that avoids market timing and is usually the one used in employee's stock purchase plans ...

*an investor though avoids this criticism if he can point to rebalancing, which I am doing, and which gets the blessings of all the investment gurus.

it is true that there is no guarantee I will see in my lifetime the same high in the stock market that we saw in mid February; younger people than I should be more sanguine as to "eventually" . As for me, I confess to being a gambler

"+EV" only applies to dollar cost averaging to the degree that it puts people to do their investing, without it too many are killed by hesitation like I described.

I have to ask you to describe what you are doing with your investments that is different?

Quote: odiousgambitQuote: OnceDearJust like rebalancing, it has value as an hedging strategy. But, I still assert it adds nothing to EV. Like Martingale, it just changes the shape of the bankroll progress chart. If it did add to EV, we could just 'double dollar average' where we spend double each time the price drops ready for the huge benefit when it rises again..... if it rises again in our lifetime.Quote: odiousgambitIt has pros and cons, but I disagree that it deserves contempt like 'hit and run'

It has advocates within the better elements of the investment community since it is a strategy that avoids market timing and is usually the one used in employee's stock purchase plans ...

*an investor though avoids this criticism if he can point to rebalancing, which I am doing, and which gets the blessings of all the investment gurus.

it is true that there is no guarantee I will see in my lifetime the same high in the stock market that we saw in mid February; younger people than I should be more sanguine as to "eventually" . As for me, I confess to being a gambler

"+EV" only applies to dollar cost averaging to the degree that it puts people to do their investing, without it too many are killed by hesitation like I described.

I have to ask you to describe what you are doing with your investments that is different?

Back in the day when I had a plan where I could put some defined amount ($18,000?) into a tax deferred plan every year, most of my colleagues would have $1500 taken out of a cash account each month. I would put the entire amount into the stock market on January 1. My money was exposed to an average annual increase of 12% while my partners who had there money sitting in some savings account were making 1% or whatever. If you have the cash, and you have the long term outlook, you should always put all your money to work as soon s possible. It was and is -EV to dollar cost average IF you are investing in something that is +EV. I believe the stock market is positive EV.

Quote: odiousgambit

I have to ask you to describe what you are doing with your investments that is different?

I play blackjack with them :o)

I tended to buy what either were discounted shares in my employer, or shares where I perceived good value. Then I hold for a long time.

The employer shares did well for me. Mixed results with stuff I chose myself.

This month, my share portfolio has taken a big hit, but fortunately, I'm mostly in cash or company bonds at the moment. I anticipate doing some adventurous trading soon, comprising some short positions for maybe 2 months. If/when the markets are 20% lower than they are now, if I survive, I'll maybe go long and hold.

I see a lot lower to go on the main indices, and don't over rate Fridays little dead cat bounce.

Time will tell.

Where I worked you couldn't do that. I tip my hat to you for doing that. All plans are good that avoid market timing.Quote: SOOPOOBack in the day when I had a plan where I could put some defined amount ($18,000?) into a tax deferred plan every year, most of my colleagues would have $1500 taken out of a cash account each month. I would put the entire amount into the stock market on January 1. My money was exposed to an average annual increase of 12% while my partners who had there money sitting in some savings account were making 1% or whatever. If you have the cash, and you have the long term outlook, you should always put all your money to work as soon s possible. It was and is -EV to dollar cost average IF you are investing in something that is +EV. I believe the stock market is positive EV.

Did you or do you ever rebalance?Quote: OnceDearI play blackjack with them :o)

I tended to buy what either were discounted shares in my employer, or shares where I perceived good value. Then I hold for a long time.

The employer shares did well for me. Mixed results with stuff I chose myself.

This month, my share portfolio has taken a big hit, but fortunately, I'm mostly in cash or company bonds at the moment. I anticipate doing some adventurous trading soon, comprising some short positions for maybe 2 months. If/when the markets are 20% lower than they are now, if I survive, I'll maybe go long and hold.

I see a lot lower to go on the main indices, and don't over rate Fridays little dead cat bounce.

Time will tell.

I used to have 3 and 5 year 'Sharesave schemes' which were absolute no-brainers. I maxed those out and as each matured, I'd unload and pay chunks off my mortgage. When I left work, I was very 'overweight' in shares in that one business*, so I unloaded as many as I could, short of crystalising taxable gains, and then I spread funds across about 10 FTSE stocks. After that, I had a few years in other employment and maxed out tax avoiding pension contributions. Now, I'm rather in draw-down mode, not seeking much more than a secure retirement.Quote: odiousgambitWhere I worked you couldn't do that. I tip my hat to you for doing that. All plans are good that avoid market timing.

Did you or do you ever rebalance?

Not much point taking risks if that means I either die richer or die poor. But I will take a rare punt soon for s**ts and giggles.

Recently, the shares in my ex-employer have been absolutely slaughtered in the market, so my diversifying paid off to the extent I did so.

49% cash (not including 1yr expenses emergency fund)

17% international stocks

21% bonds

14% us stocks

- probably going to add 8% to intl stock fund on mon, no matter how the market does. (All in ira acct)

- want to add 4% to total bond fund in ira acct but from odiousgambit advice, not going to add any right now. (But when will be the right time to add?)

- for total stock market fund, will wait till my '3up days' signal then dollar cost avg for 3 weeks. (vtsax in ira acct, rest in Fidelity's 0% expense ratio FZROX in taxable acct)

As the small investor gets squeezed, cash become king, MHA is sell bonds at their near-peak here. As Treasury rates go to zero cash becomes the better economic power.

I'm a take-your-nickle-and-go-home investor, 55% Divi-Stock 45% cash. Cover/exchange if needed.

JMHO

Suited89

can someone explain to me what 'fed funds rate of zero' means in simple English?

Also...... I own one bond paying 4.25% with a maturity date of 2026. With our near zero interest rates that bond should be worth 112 or so. But listed at 90! FORD.

I think the smart ones are expecting Ford to go bankrupt.

Also.... futures looking to stock market collapse tomorrow.

no idea what FED 0% rate means except that my bank acct interest will drop to near 0% also. :(Quote: SOOPOOtwo questions or comments.....

can someone explain to me what 'fed funds rate of zero' means in simple English?

Also...... I own one bond paying 4.25% with a maturity date of 2026. With our near zero interest rates that bond should be worth 112 or so. But listed at 90! FORD.

I think the smart ones are expecting Ford to go bankrupt.

Also.... futures looking to stock market collapse tomorrow.

this is my understanding about bonds:

if your bond is from Ford, then it's a corporate bond.

while lowering of interest rates will make it worth more, people are also not valuing the bond that highly because of the risk it could fall into junk bond territory.

there are better paying junk bonds out there.

if you plan to hold it till maturity, then it doesnt matter. you'll get paid the 4.25% interest (unless the company goes bankrupt, even if it restructures).

Zero-Coupon bonds (buy at discount, redeem at face value... its capital gain not interest)

Commercial Bonds (Ford, GM, IGT, et al usually rated AA through junk)

T-Bills ($100,000 face value usually 90 days)

Treasuries (common Federal issued investment bonds, 10 year at less than 1% at present)

Municipals (issued by State/City to finance projects, most have a simple description attatched to the bond [ General Obligation, Transportation, etc]}

Insured Municipals

Some bonds are collateral-backed, some not. To make it more complicated, some preferred stocks are bonds in disguise (prevalent in the Mortgage industry).

But the REAL intrest rate that needs adjusting is the CREDIT-CARD interest rate. That, IMHO, needs a cap of 15%. Enuff of this 5 to 4 with cash-back and points.

Regards

Suited89

Interesting how the markets react to news. On Friday, national emergency is declared (sounds like bad news?), now fed funds rate is dropped (sounds like good news?). Yet the market reactions are the oppositeQuote: unJonLooks like market set for a bloodbath tomorrow.

In times of crisis, it seems no matter what the government does or says...it won�t halt a collapsing market for more than a day or two. Friday might have been last chance to sell before the bottom falls out. Time will tell