Baccarat Side Bet Counting

Quote:

“If the gambler has zero edge, then the criterion recommends the gambler bet nothing.”

If the edge is negative, you do other activities. This is ridiculous!

The correct theory for gambling is expected utility theory, as suggested by many mathematical economists.

In the intro it says explicitly “The practical use of the formula has been demonstrated for gambling”

I am not going to do this for at least a year, I still have to add Pai Gow Tiles / Poker to my website…

knowing about them versus actually making money from them are two different things.Quote: acesideI haven’t read the whole thing. Will do later. Again, I know side bets better than many above posters here do. Trust Eliot professor of side bets.

link to original post

Quote: harrisTheoretical math is cool and everything but someone should make a program that simulates being a baccarat counter over a million shoes to see the real expected gain

I am not going to do this for at least a year, I still have to add Pai Gow Tiles / Poker to my website…

link to original post

BTW, I recommend Stanford Wong's book on Pai Gow Poker. His basic strategy for PGP is a good read.

Quote: harrisTheoretical math is cool and everything but someone should make a program that simulates being a baccarat counter over a million shoes to see the real expected gain

I am not going to do this for at least a year, I still have to add Pai Gow Tiles / Poker to my website…

link to original post

The gains can be calculated out analytically. No simulation is even needed. Again, reference Eliot.

Quote: GrahamThorpQuote: acesideHow is SCORE related to side bets? Trust Eliot Jacobson Professor of side bets. He has a math degree. He knows this stuff much better.

link to original post

He obviously does not, unfortunately. No one should be taking anything Eliot Jacobson says on trust, he is simply, demonstrably wrong.

It really should be obvious there is a major problem here.

He is recommending you bet $100 on a 40-1 proposition with as little as a 1% edge, The bankroll you would need to do that betting Kelly is $400,000.

You can do the calculation yourself. You don't need to trust anybody.

To find the Kelly fraction, type this exactly into a calculator:

(40 × 0.024634 - 0.975366) ÷ 40

Which gives you 0.00025 — that is the fraction of your bankroll you should bet.

To get the win probability (0.024634) in the first place, type:

1.01 ÷ 41

And to get the losing probability (0.975366) type:

1 - 0.024634

Finally, to find the bankroll required to make $100 the correct bet, type:

100 ÷ 0.00025

Which gives $400,000

SCORE is simply the return on a 10k bankroll betting Kelly. It is designed to be used for any advantageous gambling situation.

People use SCORE to accurately assess the value of a given wager. What SCORE does very well and edge does not is adjust for risk.

In this case it clearly shows the Dragon 7, Panda 8 and most other baccarat side wagers to be a complete waste of time for card counting purposes. We should expect this. Casinos hire mathematicians themselves to run the numbers. They do make mistakes but not that often.

link to original post

"(40 × 0.024634 - 0.975366) ÷ 40

Which gives you 0.00025 — that is the fraction of your bankroll you should bet."

What is the purpose of dividing by 40? If it's a 1% advantage, you should bet 1% divided by the standard deviation. I get 6.35 for that, so my bankroll would need to be $63,500.

BR = bankroll required = Bet size *Var / ev / k = 100*40.37/0.01/1 = $403,700.

Bet size = ev / Var * BR * k

After every round, your ev , Var and BR will change, you should adjust your bet size according to the above formula in order to maintain ROR = 13.53%.

I will show the simulation results later.

Edited.

Quote: KevinAAQuote: GrahamThorpQuote: acesideHow is SCORE related to side bets? Trust Eliot Jacobson Professor of side bets. He has a math degree. He knows this stuff much better.

link to original post

He obviously does not, unfortunately. No one should be taking anything Eliot Jacobson says on trust, he is simply, demonstrably wrong.

It really should be obvious there is a major problem here.

He is recommending you bet $100 on a 40-1 proposition with as little as a 1% edge, The bankroll you would need to do that betting Kelly is $400,000.

You can do the calculation yourself. You don't need to trust anybody.

To find the Kelly fraction, type this exactly into a calculator:

(40 × 0.024634 - 0.975366) ÷ 40

Which gives you 0.00025 — that is the fraction of your bankroll you should bet.

To get the win probability (0.024634) in the first place, type:

1.01 ÷ 41

And to get the losing probability (0.975366) type:

1 - 0.024634

Finally, to find the bankroll required to make $100 the correct bet, type:

100 ÷ 0.00025

Which gives $400,000

SCORE is simply the return on a 10k bankroll betting Kelly. It is designed to be used for any advantageous gambling situation.

People use SCORE to accurately assess the value of a given wager. What SCORE does very well and edge does not is adjust for risk.

In this case it clearly shows the Dragon 7, Panda 8 and most other baccarat side wagers to be a complete waste of time for card counting purposes. We should expect this. Casinos hire mathematicians themselves to run the numbers. They do make mistakes but not that often.

link to original post

"(40 × 0.024634 - 0.975366) ÷ 40

Which gives you 0.00025 — that is the fraction of your bankroll you should bet."

What is the purpose of dividing by 40? If it's a 1% advantage, you should bet 1% divided by the standard deviation. I get 6.35 for that, so my bankroll would need to be $63,500.

link to original post

I think should divide by VARIANCE

Quote: acesideQuote: harrisTheoretical math is cool and everything but someone should make a program that simulates being a baccarat counter over a million shoes to see the real expected gain

I am not going to do this for at least a year, I still have to add Pai Gow Tiles / Poker to my website…

link to original post

The gains can be calculated out analytically. No simulation is even needed. Again, reference Eliot.

link to original post

The expected gain in his book are calculated based on a fixed bet of $100, which is not quite right.

Quote: ssho88Quote: acesideQuote: harrisTheoretical math is cool and everything but someone should make a program that simulates being a baccarat counter over a million shoes to see the real expected gain

I am not going to do this for at least a year, I still have to add Pai Gow Tiles / Poker to my website…

link to original post

The gains can be calculated out analytically. No simulation is even needed. Again, reference Eliot.

link to original post

The expected gain in his book are calculated based on a fixed bet of $100, which is not quite right.

link to original post

I do not take practical advantage play advice from anyone who is not an active and successful player. I would consider theoretical advantage play advice from a former successful player.

But I take no advantage play advice from someone who is neither.

Quote: acesideOn the wiki page of Kelly Criterion, Standard Deviation (SD) or variance does not get into the equations at all. All you need are these two things: edge and payout odds.

link to original post

The above example DRAGON 7 has only one odds (40 to 1). What if a side bet like the "Player Dragon Bonus" has multiple winning odds?

https://www.riverscasino.com/desplaines/casino/table-games/baccarat#:~:text=Dragon%20Bonus%20are%20Player%20or,1%20on%20their%20side%20wager

Quote: ssho88

I think should divide by VARIANCE

Edge/var is a perfectly acceptable approximation of Kelly. It is commonly used in blackjack because it isn't obvious how to calculate the average payout due to splits/dd's/bj etc.

With Dragon 7 the payout is always 40 so there is no need to use an approximation. Dividing by 40 is slightly more accurate than edge/variance.

None of this makes much difference however to the fact that betting $100 on every advantage is over-betting your bankroll and risking eventually certain ruin, as Jacobson actually recommends. It is very dangerous advice which is why I felt the need to speak up.

Quote: GrahamThorpQuote: ssho88

I think should divide by VARIANCE

Edge/var is a perfectly acceptable approximation of Kelly. It is commonly used in blackjack because it isn't obvious how to calculate the average payout due to splits/dd's/bj etc.

With Dragon 7 the payout is always 40 so there is no need to use an approximation. Dividing by 40 is slightly more accurate than edge/variance.

None of this makes much difference however to the fact that betting $100 on every advantage is over-betting your bankroll and risking eventually certain ruin, as Jacobson actually recommends. It is very dangerous advice which is why I felt the need to speak up.

link to original post

Thats the reason I use this formula for bet size, Bet size = ev / Var * BR * k

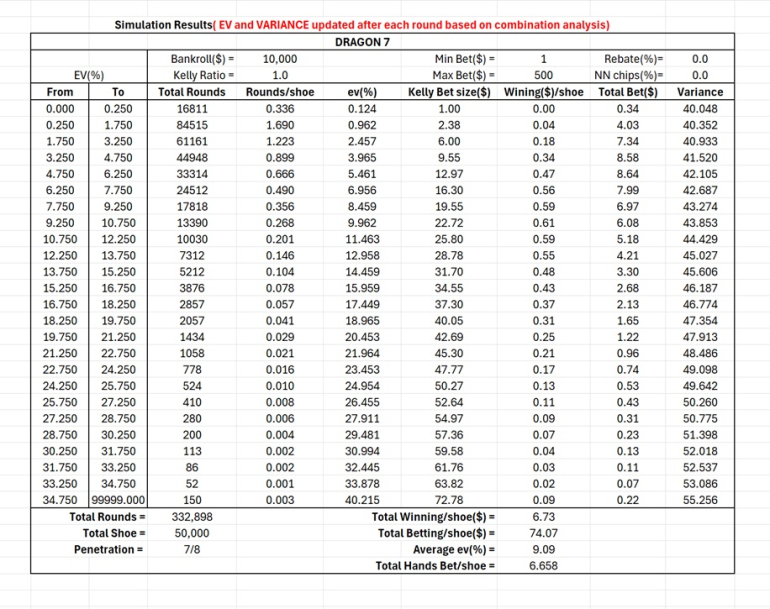

Here are the sim results of my old program (based on combination analysis after each round).

50000 shoes, penetration 7/8, kelly=1, no rebate, cash chip(No NN chip). Sim results shown that winning/shoe for TC and RC system is slightly lower.

Quote: acesideI've studied this matter a little more, but I still believe that I would bet $100 on Dragon 7 if this bet is allowed. Here is my reasoning. In this case, the only payout is 40, and the corresponding variance is about 37. However, the calculation for the variance=37 is based on the random betting situation, which does not apply to card counting. After card counting, you play the Dragon side bet only on 10% of all bet situations, that means, your variance will drop 90%. Therefore, the new variance will be 10%x37=3.7. Does this make sense?

link to original post

Interesting point. Let's pretend that you always bet $100 on a side bet, but 90% of the time, you choose this "null Dragon 7" bet which is always a push. Yes, you would be reducing the variance, but you are also reducing your edge. Instead of +1%, now it's only +0.1% because 90% of your bets have a zero edge to it. The Kelly calculation ends up being the same, with the 1/10 in both the numerator and denominator canceling each other out.

Quote: acesideI've studied this matter a little more, but I still believe that I would bet $100 on Dragon 7 if this bet is allowed. Here is my reasoning. In this case, the only payout is 40, and the corresponding variance is about 37. However, the calculation for the variance=37 is based on the random betting situation, which does not apply to card counting. After card counting, you play the Dragon side bet only on 10% of all bet situations, that means, your variance will drop 90%. Therefore, the new variance will be 10%x37=3.7. Does this make sense?

link to original post

I think you are talking about variance per shoe, I guess it is not quite right.

Player can go bankrupt after each round, so variance per round is more representative of the true situation ?

At or above Tc, player average edge is about 8%, and the hand potion is about 10%;

Below Tc, player average edge is about -9.3%, and the hand potion is about 90%.

If we bet flat one unit all the way, the overall edge is -7.6% and the variance is 37.

However, if we selectively bet only at or above Tc, the variance is probably 36. Using these numbers, what would be the Kelly wager?

Quote: acesideI need to revise my numbers. Consider card counting Dragon 7 using Eliot’s system. There is a trigger count, Tc.

At or above Tc, player average edge is about 8%, and the hand potion is about 10%;

Below Tc, player average edge is about -9.3%, and the hand potion is about 90%.

If we bet flat one unit all the way, the overall edge is -7.6% and the variance is 37.

However, if we selectively bet only at or above Tc, the variance is probably 36. Using these numbers, what the Kelly wager would be?

link to original post

Disagree, if bet above Tc, the variane should more than 37, I guess more than 40.

My above sim results shown that when ev > 0, the variance > 40, I am quite confident about the sim results, but I cannot guarantee it.

Quote: GrahamThorpAlso your comment is not consistent with an earlier observation in an article you wrote where you directly contradict yourself. From your analysis of the Lucky 6 side bet:

"Counting the Lucky 6 is, for all practical purposes, a waste of time. This is under the liberal pay table and shuffling rules. Obviously, it gets even worse with the stingier pay table or more shallow placement of the cut card. Counting the Dragon 7 or Panda 8 would be more profitable, but those are also a waste of time. There are much more profitable ways for the advantage player to make money."

The Dragon 7 and Panda 8 cannot be both "very countable" and "a waste of time". As it turns out the SCORE from both is cents per hour. There is nothing here of any value.

link to original post

Touche! Good post. What changed my mind somewhat is I met with the owner of a large casino, which shall remain nameless, who said they got hit hard by a team counting the Dragon 7. At the time I made my first comment I probably thought the max bet was $25. However, at $100, I think it would entice some players/teams. The advantage is there, but it's a very volatile play.

Quote: ssho88

Thats the reason I use this formula for bet size, Bet size = ev / Var * BR * k

Here are the sim results of my old program (based on combination analysis after each round).

50000 shoes, penetration 7/8, kelly=1, no rebate, cash chip(No NN chip). Sim results shown that winning/shoe for TC and RC system is slightly lower.

link to original post

One more thing. Did you use Eliot’s system

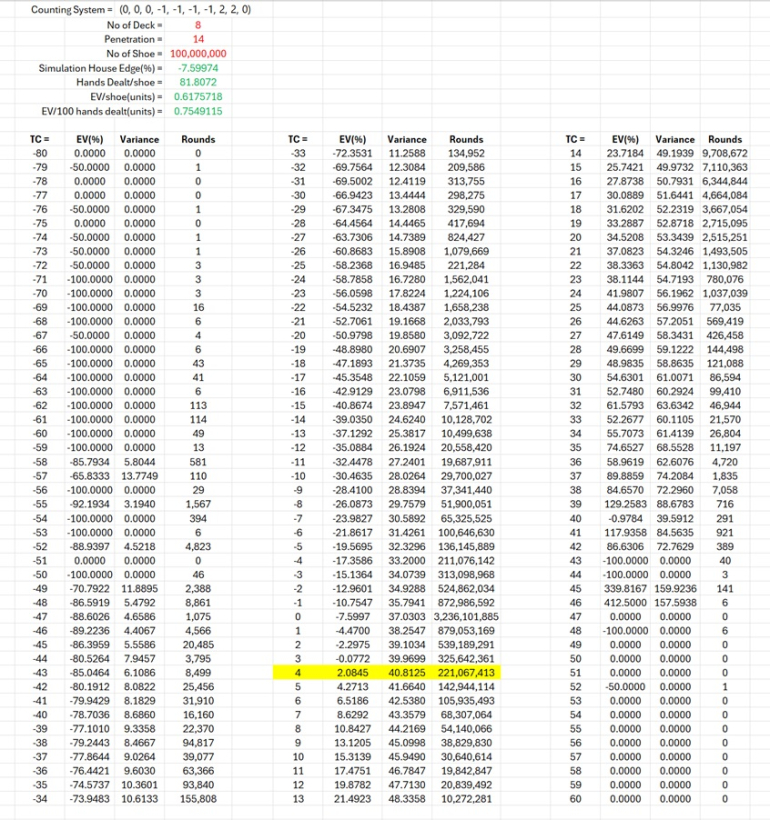

(0, 0, 0, -1, -1, -1, -1, 2, 2, 0) for cards from Ace to Ten to do this card counting simulation? Also, do you still have these values when EV numbers are negative?

Quote: acesideQuote: ssho88

Thats the reason I use this formula for bet size, Bet size = ev / Var * BR * k

Here are the sim results of my old program (based on combination analysis after each round).

50000 shoes, penetration 7/8, kelly=1, no rebate, cash chip(No NN chip). Sim results shown that winning/shoe for TC and RC system is slightly lower.

link to original post

One more thing. Did you use Eliot’s system

(0, 0, 0, -1, -1, -1, -1, 2, 2, 0) for cards from Ace to Ten to do this card counting simulation? Also, do you still have these values when EV numbers are negative?

link to original post

I used a more complex counting system that covers all positive and negative EVs.

I can re-simulate the game using the system (0, 0, 0, -1, -1, -1, -1, 2, 2, 0).

To be more precise, the trigger Tc should be 3.05, instead of 4.

Average EV = 8.03%;

Variance = 43.24;

Bet Frequency = 9.16%;

Trigger TC = +4.

So, I would say this side bet is very countable.

Now that it's been established that baccarat side bet counting is real and has been a threat to casinos, does anyone think I should pursue this project further? Or should I focus more on my website? Or does anyone have another idea reflecting some need regarding casino math that I should be looking into?

Quote: acesideGreat! It seems to me that your results agree with Eliot’s online numbers:

Average EV = 8.03%;

Variance = 43.24;

Bet Frequency = 9.16%;

Trigger TC = +4.

So, I would say this side bet is very countable.

link to original post

1) A more complex counting system(human feasible)) will give EV/100 hands dealt = 0.798 units

2) Using Combination Analysis to calculate EV after each round(not human feasible)) will give EV/100 hands dealt = 0.90+-, about 20% higher than 0.755 !

We normally use method 2) to play online casino games, LOL !

Quote: acesideGreat! It seems to me that your results agree with Eliot’s online numbers:

Average EV = 8.03%;

Variance = 43.24;

Bet Frequency = 9.16%;

Trigger TC = +4.

So, I would say this side bet is very countable.

The issue is not with Jacobson's numbers. It was what he was doing with them.

If you bet $100 every time you have an edge you will bust out a $10,000 bankroll 42% of the time before doubling. This is easy to simulate. Anybody actually trying this will very likely lose their entire bankroll sooner or later. That is what Jacobson recommends: over-betting your bankroll and losing all your money.

You need a $50,000 bankroll to win at the rate of $59 per hour and you would still have a 13% chance of going broke, which is still high for a professional player. It will take you 847! hours on average to double your bankroll. This is not in question: the only other analyst who did a study on this: Stephen How, at discount gambling, produced exactly the same numbers.

SSho88's analysis does not challenge any of that, he's trying to develop a better count system, but that neither addresses nor challenges the central problem: the bet is too risky to count.

Penetration = 402/416

Hands dealt per shoe = 81.80

Table limits = min $5 to max $500

Bankroll = $50k

Time/ shoe = 1.5 hours

1) Counting method : Perfect combinations analysis

Betting Frequency = 9.5 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $450, average betsize = $83)

Profit/shoe = $132++

ROR = 13.5%

Win rate : $88/hour

2) Counting method : Better TC system, bet when TC > 11

Betting Frequency = 9.3 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $410, average betsize = $75)

Profit/shoe = $96++

ROR = 13.5%

Win rate : $64/hour

3) Counting method : Eliot's TC system, bet when TC > 4

Betting Frequency = 7.6 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $440, average betsize = $87)

Profit/shoe = $91++

ROR = 13.5%

Win rate : $61/hour

Quote: ssho88Here are my stats:

Penetration = 402/416

Hands dealt per shoe = 81.80

Table limits = min $5 to max $500

Bankroll = $50k

Time/ shoe = 1.5 hours

1) Counting method : Perfect combinations analysis

Betting Frequency = 9.5 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $450, average betsize = $83)

Profit/shoe = $132++

ROR = 13.5%

Win rate : $88/hour

2) Counting method : Better TC system, bet when TC > 11

Betting Frequency = 9.3 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $410, average betsize = $75)

Profit/shoe = $96++

ROR = 13.5%

Win rate : $64/hour

3) Counting method : Eliot's TC system, bet when TC > 4

Betting Frequency = 7.6 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $440, average betsize = $87)

Profit/shoe = $91++

ROR = 13.5%

Win rate : $61/hour

link to original post

Thanks for directly addressing my point about risk and providing the data.

In case there were any doubt I believe your numbers to be accurate, For a $50,000 bank, I got $73 per hour based on a human count system betting Kelly which is close enough to your numbers to be attributable to methodological differences.

A benchmark blackjack game would have a SCORE of 50, that is a return of $50 per hour betting Kelly on a 10k bankroll. This represents a return of $250 per hour on a 50k bankroll. By comparison your numbers show the Dragon 7 to be over 400% worse than a mediocre count game. So most advantage players would simply count cards at blackjack at almost any game they could find, it would generally be significantly better.

Realistically if any one did actually try this they don't pose enough of a threat to the casinos to justify any kind of countermeasures. The countermeasures would almost certainly cost the casinos vastly more than they saved from this largely non-existent threat. By an order of magnitude, it is not close.

On combinatorial analysis:you can get a better ROI from the main wagers with computer-perfect play. It might be interesting if you could do BOTH but I don't know of anywhere where using a computer is legal.

Quote: GrahamThorp

If you bet $100 every time you have an edge you will bust out a $10,000 bankroll 42% of the time before doubling. This is easy to simulate.

link to original post

I have a question about the definition of Kelly bust-out probability. Why is “before doubling” in this definition? My understanding is that the probability is calculated with an infinite time of playing only positive edge situations.

Can somebody confirm this part?

My calculated ROR is 40.80%.

Quote: ssho88We do use combinatorial analysis in online casino to analyze both main bets & side bets, and bet accordingly, unfortunately, the ROI of the main bet(BANKER/PLAYER) is very low.

link to original post

By main wagers I meant bank, player and tie. And it is mostly tie hence the confusion.

Others describe the main wagers as player and bank with the tie treated as a side-bet. Because the tie exists in almost every traditional baccarat game I use the former definition. The latter definition is not unreasonable,

Though I think it is important to emphasize the bank and player bets can have very high maximums-one of a few reasons to accept a much lower SCORE.

Quote: aceside

I have a question about the definition of Kelly bust-out probability. Why is “before doubling” in this definition? My understanding is that the probability is calculated with an infinite time of playing only positive edge situations.

Many serious professionals work to a global 1% risk of ruin, you are correct. Losing their bank is catastrophic when you have no other means of support like a job so they are much more conservative than the numbers we are using. This is how I actually bet.

The reason I used ror before doubling in this case is to give a simple example of how Jacobson recommends you should dangerously overbet your bankroll. Any one can repeat that experiment and observe how high the ROR is.

The phenomena ssho88 is referring to is called "premature bumping into the barrier syndrome". It was developed to help people decide how much money to bring on a trip. Schlesinger warns people that you can't calculate your chance of losing a trip bankroll on the basis of an endpoint calculation over n hands because you might lose your bankroll before you get to the end of the trip. It is a useful concept.

Also, the majority of the bet opportunities exist only at the very end of a few advantage shoes. They are not randomly distributed in random shoes. Therefore, Kelly is not very correct here.

Quote: acesideWe have to consider if Kelly Criterion is really applicable to side bets or not. Let’s use ssho88’s bet frequency of 7.6 hands per shoe to investigate the Dragon 7 side bet. A player can play three Baccarat shoes a day and five days a week. This means that this player can play 7.6x3x5x52=5,928 hands a year. The total wager is only $592,800.

Also, the majority of the bet opportunities exist only at the very end of a few advantage shoes. They are not randomly distributed in random shoes. Therefore, Kelly is not very correct here.

link to original post

No, Kelly applies to everything.

But because of the long time periods (on a human scale) involved, and the fact that we are doing other things with our money, playing other games, having expenses and sources of income rather than just being a machine playing a probabilistic game, we can treat concepts like "full Kelly" and "half Kelly" differently. For example if I decide I don't like the way a particular high variance campaign has been treating me, I can go do something else. Or I can lower my stakes until my luck turns around. Some players (slightly more than 1 out of 40!) will hit a bet like that the first time they play it with an advantage, and then all their math changes. Or if you can only afford 2 bets, then you may be one of the lucky 5% who hits it within 2 hands. Then you can afford a whole bunch of bets.

And one of the things Kelly's Theorem doesn't address is the chances that we will find a better game.

Quote: ssho88Here are my stats:

Penetration = 402/416

Hands dealt per shoe = 81.80

Table limits = min $5 to max $500

Bankroll = $50k

Time/ shoe = 1.5 hours

3) Counting method : Eliot's TC system, bet when TC > 4

Betting Frequency = 7.6 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $440, average betsize = $87)

Profit/shoe = $91++

ROR = 13.5%

Win rate : $61/hour

link to original post

Hi, I’m learning about Kelly wager, but Don never had the patience to teach me this. You are my mentor.

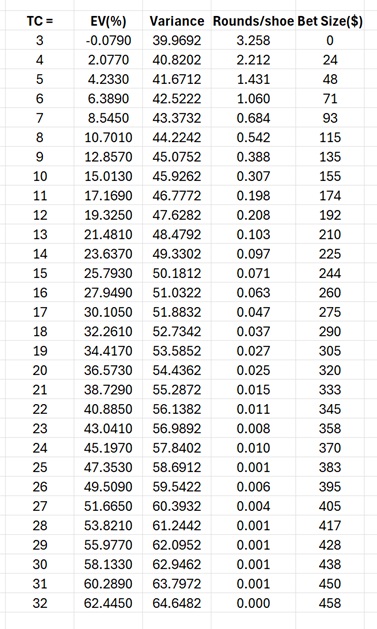

In this particular example above, how do you find the maximum wager of $440? The edge increases quickly with the count, but variance increases slowly. So, what is your criterion to set this bet spread of $5-$440?

Quote: acesideQuote: ssho88Here are my stats:

Penetration = 402/416

Hands dealt per shoe = 81.80

Table limits = min $5 to max $500

Bankroll = $50k

Time/ shoe = 1.5 hours

3) Counting method : Eliot's TC system, bet when TC > 4

Betting Frequency = 7.6 hands/shoe

Bet size : 1 kelly (bet size range from $5 to $440, average betsize = $87)

Profit/shoe = $91++

ROR = 13.5%

Win rate : $61/hour

link to original post

Hi, I’m learning about Kelly wager, but Don never had the patience to teach me this. You are my mentor.

In this particular example above, how do you find the maximum wager of $440? The edge increases quickly with the count, but variance increases slowly. So, what is your criterion to set this bet spread of $5-$440?

link to original post

Simulation

However, you say $61 per hour when using a bet spread of $5-$440. That means, your profit is about $61x1.5=$91.5 per shoe. This does not sound correct, because your average bet is $87, less than Eliot’s $100. Could you explain this?

Quote: acesideI re-read Eliot’s online article again and found a little discrepancy between his dollar amount and yours. Eliot says: if a counter flat bets $100 whenever there is an edge, then he will average about $59.67 profit per shoe.

However, you say $61 per hour when using a bet spread of $5-$440. That means, your profit is about $61x1.5=$91.5 per shoe. This does not sound correct, because your average bet is $87, less than Eliot’s $100. Could you explain this?

link to original post

It is because betsize adjust according to kelly betsize, when higher ev, bet higher amount, but average betsize still can be smaller than $100.

1) Kelly bet size, average betsize = $87, profit/shoe = 91.5

2) Flat bet size, average betsize = $100, profit/shoe = 59.67

Conclusion, Kelly betting is much more efficient.

Its been proven beyond a doubt that Kelly is applicable to gambling. I have a question for you. Do you actually play or is this just a hobby of yours. Your posts seem to be obtuse whether intentional or not.Quote: acesideActually, you are very knowledgeable! I’ve learned a lot things from you. Thank you for your patience! I’ll put these numbers into my laptop later. In the meantime, I just want to say that this is a perfect example for demonstrating if Kelly is really applicable to gambling or not. Kelly is based on infinite time playing of positive edge situations only. What is infinite? I guess many billions of hands, to say the least; however, we are concerned here with only several thousand hands. My understanding is Kelly is not applicable here.

link to original post