What are your investing thoughts

Good financial advice doesn't cost. It pays.

I.B.D. Rinse and repeat for generational wealth.

I fired one a long time ago that my wife had already when I got married. He worked for a division of American Express before it was called Ameriprise. They got into trouble for guiding clients into funds that were good for them and bad for the client, a conflict of interest thing. After he left them he was still trying to get us into crappy funds you never heard of, it's like it was what he learned and all he knew. My wife finally agreed with me that he was an idiot after he was pushing hard to get us into real estate just before the real estate crash in the 2000s.

Financial advisors are salesmen, not money gurus.

Number one rule of Wall Street.

Nobody...

I don't care if you're Warren Buffett or if you're Jimmy Buffett.

Nobody knows if a stock is gonna go up, down, sideways, or in f'ing circles.

Least of all stockbrokers.

1) Never lose money on an investment

2) Never forget Rule #1

You want to raise rates�DO IT.

Stop with the nonstop �its coming�. �It�s gonna happen�. �Soon enough�. �Maybe in a month�.

All he does is roil markets.

tuttigym

IMO, it�s knowing when to sell that�s the hard part, because there can be sizable pullbacks even in the middle of a bull market. But after a true crash (50%), once you see prices have gone up 20%, you can be almost certain the bear market is overQuote: odiousgambitIt's not good enough to time it so that you sell at near top-market, which takes some luck. You also have to get back in at the right time. Market timing has consistently been shown to be a loser, mostly because of this second factor. People simply screw it up.Quote: Ace2No one can time the market exactly

But one thing is for sure: bull markets always come to an end. And this one has been going strong for ten years, especially the last 3-5. This sudden, near 10% drop in the S&P is not normal for this super bull market

Traditional valuations show the market extremely overpriced�maybe more than ever before. Of course the market could continue going up a bit more, but how much more insanely overvalued can it get. I believe that if you sell now, it will probably look like a very smart decision within a year, if not sooner

link to original post

link to original post

A couple days ago, my 10% trailing stop loss orders (that I set up about a year ago) did execute, so a portion of my holdings sold.

I�m not normally a market timer�I�ve been 80%+ invested for decades. However, I�ve never seen the market so incredibly overpriced, and it�s not just me saying that. I guess what�s changed is I�m not as young as I used to be and therefore not as willing to wait a long time for the market to recover after a potential crash.

I made a ton of money over the last several years (especially the last three years) but something is telling me that now would be a great time to cash out some of those profits. So maybe I don�t see this as market timing�more like you have to start taking your money out of the market sometime. What�s the point of staying fully invested until you die

One problem with selling is that your proceeds earn essentially zero interest. Makes it even harder to sell but that�s one of the main reasons the stock (and real estate) markets are so inflated. But the rock bottom interest rates can�t and won�t last forever

The "data" says inflation is 7%, yet the fed funds rate is 0%, and the fed is still buying bonds.

Quote: Gundy

The "data" says inflation is 7%, yet the fed funds rate is 0%, and the fed is still buying bonds.

They could be buying more than bonds. Directly or indirectly. They have a trading desk on the NY Exchange. We saw that 1,000 point swing a few days ago. Overnight the Futures were down 1,000 until there was a quick 1,000 point turnaround beginning at 2AM.

Not that I'm complaining.

Recent inflation data makes it seem like the Fed will have to raise rates substantially�huge spike in inflation. That would cause all asset bubbles to deflate, especially real estate

Who knows, maybe Dow will hit 60,000 before it reverts back to a normal valuation. Could actually happen but I say we�ll see 20k before 60k. And 20k would still be overvalued based on average historical market cap to GDP ratio

Quote: odiousgambitDow down 1000 pts but climbing back up at the moment

my kind of plan doesn't go into action yet, has to get below 30,000 ... really more like 28,000

yes it means this is not yet a crash

link to original post

I'm keeping an eye on it now for sure. A few minutes ago Dow dipped below 33,000

Quote: odiousgambitQuote: odiousgambitDow down 1000 pts but climbing back up at the moment

my kind of plan doesn't go into action yet, has to get below 30,000 ... really more like 28,000

yes it means this is not yet a crash

link to original post

I'm keeping an eye on it now for sure. A few minutes ago Dow dipped below 33,000

link to original post

My investment in XOM (Exon) has almost doubled and continues to "outperform" the market. I believe I mentioned this stock prior to the first of 2022. When it hits my target price, even if there is still growth available, I will sell without any tax consequences. It is in my IRA.

tuttigym

It probably still would have been, but now we have the possibility of Russia attempting to retake E Europe, and who knows what else. The market hates uncertainty and it doesn't take much to reverse bullish sentiment and pop a bubble.

I'm shocked that the Dow is still above 30k.

Quote: Ace2The market was up intraday but could not hold a gain, which is one of the hallmarks of a bear market. This has happened many times over the last couple months.

link to original post

Nothing is being held into close. Everything is dumping and it�s been like this for a while now. Short traders must be making a killing shorting everything in sight in the last 30 minutes and closing the position at 3:59pm. Rinse, repeat.

Quote: Ace2Recent inflation data makes it seem like the Fed will have to raise rates substantially�huge spike in inflation. That would cause all asset bubbles to deflate, especially real estate.

Not exactly "all asset bubbles." Many investors, especially retirees, are heavily into bonds. For anyone around in the 70's, the 14 percent or so interest rates still draw a smile.

14 percent interest and inflation was probably 10 percent. Take out 30% taxes and it's a net loss in real termsQuote: SanchoPanzaQuote: Ace2Recent inflation data makes it seem like the Fed will have to raise rates substantially�huge spike in inflation. That would cause all asset bubbles to deflate, especially real estate.

Not exactly "all asset bubbles." Many investors, especially retirees, are heavily into bonds. For anyone around in the 70's, the 14 percent or so interest rates still draw a smile.

link to original post

If you already own bonds at a fixed interest rate, doesn't a rate hike make their value decline? Inverse relationship between interest rate and bond price

Quote: Ace214 percent interest and inflation was probably 10 percent. Take out 30% taxes and it's a net loss in real termsQuote: SanchoPanzaQuote: Ace2Recent inflation data makes it seem like the Fed will have to raise rates substantially�huge spike in inflation. That would cause all asset bubbles to deflate, especially real estate.

Not exactly "all asset bubbles." Many investors, especially retirees, are heavily into bonds. For anyone around in the 70's, the 14 percent or so interest rates still draw a smile.

link to original post

If you already own bonds at a fixed interest rate, doesn't a rate hike make their value decline? Inverse relationship between interest rate and bond price

link to original post

Ten percent isn't exactly chopped liver. Nor is 30% tax rate, when the overwhelming number of retirees are in the 20 to 30% range. Besides, check out this statement and tell us which stocks had higher returns in that time period:

"Interest rates reached their highest point in modern history in 1981 when the annual average was 16.63%, according to the Freddie Mac data. Fixed rates declined from there, but they finished the decade around 10%. The 1980s were an expensive time to borrow money."

This is no surprise since high inflation discounts the value of future earnings. And there's no reason to risk your capital in the stock market when you can get 10% from a FDIC insured savings account

I really like these charts where you can move the start and end dateQuote: SanchoPanzaQuote: Ace214 percent interest and inflation was probably 10 percent. Take out 30% taxes and it's a net loss in real termsQuote: SanchoPanzaQuote: Ace2Recent inflation data makes it seem like the Fed will have to raise rates substantially�huge spike in inflation. That would cause all asset bubbles to deflate, especially real estate.

Not exactly "all asset bubbles." Many investors, especially retirees, are heavily into bonds. For anyone around in the 70's, the 14 percent or so interest rates still draw a smile.

link to original post

If you already own bonds at a fixed interest rate, doesn't a rate hike make their value decline? Inverse relationship between interest rate and bond price

link to original post

Ten percent isn't exactly chopped liver. Nor is 30% tax rate, when the overwhelming number of retirees are in the 20 to 30% range. Besides, check out this statement and tell us which stocks had higher returns in that time period:

"Interest rates reached their highest point in modern history in 1981 when the annual average was 16.63%, according to the Freddie Mac data. Fixed rates declined from there, but they finished the decade around 10%. The 1980s were an expensive time to borrow money."

link to original post

looks like stock market sank but soon got lower even in '82. I remember those days very well, two recessions practically back to back. Didn't own stocks, just a tough time to find work

https://www.macrotrends.net/1319/dow-jones-100-year-historical-chart

Quote: Ace2The stock market was basically flat throughout that high inflation era...I think the Dow hovered around 1,000 for like 15 years.

This is no surprise since high inflation discounts the value of future earnings. And there's no reason to risk your capital in the stock market when you can get 10% from a FDIC insured savings account

link to original post

It wasn't flat, but a 10% growth when you are at 800 is only 80 points. When the dow was 800-1500, a 100 point swing in a day was huge. Today a 2,000 point swing would be about the same.

Before the 90s, most of my growth in the stock market came from reinvesting dividends. It was during the Clintons I started getting great results. Suddenly, 40% returns weren't fantasy. I forget which two years they were, but in about 24 months, my portfolio pretty much doubled and allowed me to diversify a bit.

Splitting hairs again?Quote: billryanQuote: Ace2The stock market was basically flat throughout that high inflation era...I think the Dow hovered around 1,000 for like 15 years.

This is no surprise since high inflation discounts the value of future earnings. And there's no reason to risk your capital in the stock market when you can get 10% from a FDIC insured savings account

link to original post

It wasn't flat, but a 10% growth when you are at 800 is only 80 points. When the dow was 800-1500, a 100 point swing in a day was huge. Today a 2,000 point swing would be about the same.

Before the 90s, most of my growth in the stock market came from reinvesting dividends. It was during the Clintons I started getting great results. Suddenly, 40% returns weren't fantasy. I forget which two years they were, but in about 24 months, my portfolio pretty much doubled and allowed me to diversify a bit.

link to original post

The closing value of the Dow was 969 in 1965 and 875 in 1981. With the exception of one deep (but brief) pullback in that period, it mostly bobbled between 800 and 1000 for 16 years. I think most people would consider that flat

Quote: billryanNot the people who invested. 1000 was considered an almost mythical level. If the market was at 800 and went up 10% for the year, it would be at 880. Is that flat? To me, a flat market would mean your investment in 1965 would be worth the same in 1981. That wasn't the case. I actually bought my first two stocks in 1965. A share of Sears and a share of Xerox. My Mom taught us how to read the stock charts and how to calculate what our reinvested dividends bought us. I remember the mid-80s when my friends were all seemingly getting rich buying penny stocks no one knew anything about. I'd just started my business and was cash poor so I felt I was missing out, and then the crash came and many of my friends were over-extended, having leveraged their accounts to the max.

link to original post

Up 10% isn�t the facts as Ace2 posted. 1981 was a lower price than 1965.

if the market goes down and stays down ... I've said it before, this is what I fear. Inflation seems to play a role in those periods, sometimes deflation ...

1966 down 18.9

1967 up 15.2

1968 up 4.2

1969 down 15.2

1970 up 4.82

1971 up 6.11

1972 up 14.58

1973 down 16.58

1974 down 27.57

1975 up 38.3

1976 up 17.86

1977 down 17.27

1978 down 3.15

1979 up 4.19

1980 up 14.93

1981 down 9.23.

A long range observer may say the market was flat from 1965 to 1981, but as the year end results show,

it was quite a roller coaster for those actually invested.

all you have to do is be able to predict it. I can't find it now, but it's been shown that you can turn $10k into a million in no time at all *in any market* if you get out of stocks into cash at just the right time, and then get back in at just the right time. The more volatility the better, if you can do it.Quote: billryan1965 up 10.88

1966 down 18.9

1967 up 15.2

1968 up 4.2

1969 down 15.2

1970 up 4.82

1971 up 6.11

1972 up 14.58

1973 down 16.58

1974 down 27.57

1975 up 38.3

1976 up 17.86

1977 down 17.27

1978 down 3.15

1979 up 4.19

1980 up 14.93

1981 down 9.23.

A long range observer may say the market was flat from 1965 to 1981, but as the year end results show,

it was quite a roller coaster for those actually invested.

link to original post

It has also been shown that NO ONE can do it consistently

Quote: odiousgambitall you have to do is be able to predict it. I can't find it now, but it's been shown that you can turn $10k into a million in no time at all *in any market* if you get out of stocks into cash at just the right time, and then get back in at just the right time. The more volatility the better, if you can do it.Quote: billryan1965 up 10.88

1966 down 18.9

1967 up 15.2

1968 up 4.2

1969 down 15.2

1970 up 4.82

1971 up 6.11

1972 up 14.58

1973 down 16.58

1974 down 27.57

1975 up 38.3

1976 up 17.86

1977 down 17.27

1978 down 3.15

1979 up 4.19

1980 up 14.93

1981 down 9.23.

A long range observer may say the market was flat from 1965 to 1981, but as the year end results show,

it was quite a roller coaster for those actually invested.

link to original post

It has also been shown that NO ONE can do it consistently

link to original post

Not really. The arc of the market is always upward.

Forget timing the market. Just invest and sit back and watch your money grow. Or don't. It's your choice.

If you can't figure out how to get your money to work for you, you'll waste your life working for money.

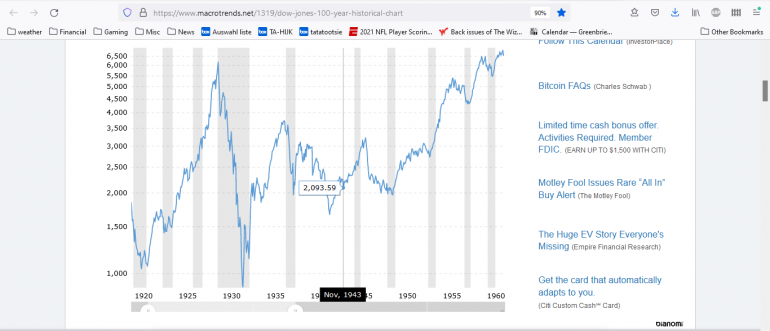

let's look at the crash of '29 using the link https://www.macrotrends.net/1319/dow-jones-100-year-historical-chart

let's look at the crash of '29 using the link https://www.macrotrends.net/1319/dow-jones-100-year-historical-chartyou can see what was going on in the 20s + 30s etc

there's no question that even a savvy investor who invested all of his money just before the crash and had ridden it out without buying or selling again would have never got his money back til the 1960s, maybe late 50s if you count dividends.

but if he had gradually dollar-costed his investments starting in 1920, maybe leary of buying during all-time highs, and didn't sell, he would have gotten back to even by the mid 30s meanwhile earning dividends. What if his heaviest buying was around the times of the recessions of the 20s and 30s?

So there is something to this thing about an 'arc' which you can see starting at 1920 through 1960. You can benefit from it if you avoid certain things, like panic. You also can't invest what you might need to cash out in 5 yrs, 10 conservatively. But you also can't be the guy who jumped into the market in 1929.

unfortunately by then you're this old fart

That's about right. The stock market (just like some other asset classes) tends run in 15-20 year cycles. 16 years of low/zero returns (or even slightly negative like 1965-1981) then 19 years of outstanding returns (up about 1000% from 1981-1999). That's about 7% average annual appreciation over that 34 year period, all of which came in the second half of it.Quote: odiousgambitI've said it before, the magic of investing kicks in after 40 years

unfortunately by then you're this old fart

link to original post

The stock market is a very long term investment and you need several decades to be reasonably confident of realizing historical average returns

I guess you didn't read the post?Quote: billryanWhat is that chart supposed to show?

link to original post

snips:

... investor who invested all of his money just before the crash ... would have never got his money back til the 1960s [this is often pointed out by those against stock investing]

... but if he had gradually dollar-cost-averaged his investments starting in 1920 ... he would have gotten back to even by the mid 30s [there are ways to reduce risk of this]

So there is something to this thing about an 'arc' [which I thought you agreed with]

... you [should] avoid certain things, like panic. You also can't invest what you might need to cash out ... you also can't be the guy who jumped into the market in 1929. [the chart shows this clearly]

this same thing can be shown for the investor who jumped into the market all at once in 1965. He was doomed to wait till 1981 for that portion of his money to come back to even. Of course a very typical reaction by what is likely to be a rookie investor is to panic in '61 or '62 , sell it all at a loss, and go around telling his kids etc never to invest in stocks

Yeah, if someone was unfortunate enough to have invested their life savings on a certain day in 1965, bought the theoretical Dow, never invested another dime and didn't reinvest his dividends he would not have broken even until 1981, although anyone with that kind of luck was most likely killed by a piece of Skylab.

It's often presented that way by the Media, at least they suggest such a thing by the way crashes are reported. I distinctly remember them repeatedly saying in 2008 that the market went back to its value it had 12 years before.Quote: billryanThe numbers in the chart seem way off. It has the Dow higher than it was.

Yeah, if someone was unfortunate enough to have invested their life savings on a certain day in 1965, bought the theoretical Dow, never invested another dime and didn't reinvest his dividends he would not have broken even until 1981, although anyone with that kind of luck was most likely killed by a piece of Skylab.

link to original post

Quote: billryanThe numbers in the chart seem way off. It has the Dow higher than it was.

link to original post

Quote: chart infoHistorical data is inflation-adjusted using the headline CPI and each data point represents the month-end closing value

whether or not you like AI or ChatGPT it has lit a fire in the tech world

in 2022 the Nasdaq 100 lost one third of its value

so far in 2023 it's up 31%

I own VGT - a Vanguard index fund that is based on tech - it's way up too - woo hoo

https://www.industryweek.com/technology-and-iiot/article/21260367/chatgpt-sparks-ai-gold-rush-in-silicon-valley

.

the S&P is now in a bull market per the common indicator - the index has risen 20% or more from its most recent low

most of the gains have come from a small group of tech stocks - and some critics say it is unsustainable

https://apnews.com/article/bull-stock-market-wall-street-cde5d042da6aa887e7d5ba64b62815ff

.