What are your investing thoughts

Quote: RaleighCrapsSo, let's see if I have this right......wouldn't the overall fund have to be in positive territory, at the 2% rate for the bonds they were holding (assuming 0% fees)?

I don't understand this perfectly, either, but you should realize you lose value only because interest rates go up after you invest. What you hold is old bonds, in funds or otherwise. The new bonds are clearly worth more, so if you sell your old bonds, they have less value vis a vis the new bonds, and go at a discount.

Still, holding on to real bonds to maturity, you need not worry, same as your house going down in value but you didnt intend to sell anyway at that time.

Holding on to a bond fund, worry LOL. People are buying and selling the fund, but I think it is a bigger factor that the fund managers do not think of holding on to the old bonds [this is the part of this I am unsure of, but ...] I believe what happens is there is value in going ahead and getting the new bonds.

Thus in your example, a well run fund would not be worth what you went in at plus 10 yrs of 2% interest, but if rates do something to make your funds go down in value, by the end of the 10 yrs you will have done better than that.

If I have learned anything, it is that you never want to be in the position of "having to sell" any quantity of stocks *or* bonds. If you can absolutely hold on to them and are well diversified just do so, rebalancing now and again. After a long enough period of time, you are going to come out smelling like a rose. Even in the worst performing [but diversified] investments, 30 years is going to make you look sweet. 40 years: it reaches mythical proportions.

You don't start a thread with this title when you are just kicking back without worries for the next 30 years though.

Last few months my broker has advocated corporate bonds with good coupon rates, but she'll only buy them at a discount. So whether they're subject to an early call or held to maturity, so there'll be a bit of appreciation plus the income stream -- as long as the company remains solvent, of course.

Recent Examples:

CINCINNATI BELL TEL DEBENTURE CPN 6.300%

MBIA INC BONDS CPN 5.700%

PULTE HOMES INC NOTES CPN 6.000%

Overseas:

TRANSOCEAN SEDCO FOREX NOTES CPN 7.450%

I don't know whether these are still trading at a discount, I don't track them daily. The whole point was to buy at a discount, pocket the income, and forget about them.

Quote: Caldermy broker has advocated corporate bonds with good coupon rates, but she'll only buy them at a discount.

Bonds trade at a discount when new issue has better rates, so I don't see how that is a factor.

Then again, I know little about corporate bonds except anyone has to realize these excellent returns are high because the default risk is high. I wouldnt be here if I didnt like gambling, but I have to know at least something about the game before I sit down to play.

Quote: mdhovlandUsing the SPY and TLT, beginning 8/31/2007, no reallocation:

50/50

Best,

Mark

same, starting at march 5th, 2009

link

Mark, how much do you know about bonds? I have some questions:

*as the 10 yr is marching toward 1% or even lower, I tend to assume that bonds will hit the wall at some point, and can only wallow in the mud at low rates or eventually interest rates will go up. Or is it like the string that keeps being cut in half? eventually a real string can't be cut in half anymore, but a theoretical string can mathematically be cut in half forever. How about bonds? [how's that for string theory LOL] What I mean is, can we go for years with bonds just continuing to go up in value, or are those days coming to an end as we approach 10 yr 1% ... supposedly the Fed wants to start increasing rates.

*some European bonds are at negative interest rates. How do they do that and can that happen with US treasuries?

I know a bit but I probably might not be of much help when it comes to “why” this is going on. I can do the math to figure YTM, OID etc., but I can’t explain precisely why investors do or don’t buy bonds or currency in situations like we are currently seeing. I know why I don’t buy them but that’s subjective.

To (ab)use an old adage, “Money goes where it is treated best.” I know that sounds trivial, but...

-----*some European bonds are at negative interest rates. How do they do that and can that happen with US treasuries?

To answer your last question first, yes. In late 2013, US 3 mo. T-bills did go negative for a very short period in the secondary market. I read someplace that Denmark had two-year notes that were ISSUED at a negative yield for in 2012 and again last fall. I think buyers might have been making an interest rate play anticipating a rate cut. Not sure. Anyway, here's how they can go negative:

If you pay $1002.50 for a stripped note or bond in the secondary market and it matures at $1000, you have a negative yield to maturity.

$1002.50 paid, $1000 returned = -$2.50 return at maturity (a loss).

-$2.50/$1000 = -.25% yield to maturity.

If a bond still has the coupon attached - as issued or even AT issue - and you pay more than the coupon and par value both generate, a negative yield will also result. (The coupon entitles the income stream. A strip doesn't.)

If one trusts the credit-worthiness of the bond issuer, they will have merely paid a “fee” for the guaranteed return of principal.

You also wrote:

-----*What I mean is, can we go for years with bonds just continuing to go up in value, or are those days coming to an end as we approach 10 yr 1%

Here again, I’m baffled. Low interest rates are supposed to foster and generate economic growth. By many accounts, this is not happening, even on a global view. Now that the US QE’s are completed, I’m beginning to notice headlines of European QE.

We’ve been bouncing along the bottom for several years already with T-bills at lows of 5/8% yield and the USD at less than 1/10th% here and there. While the dollar has risen lately (especially against other currencies), I won’t even try to make a forecast on how this all plays out.

Kind of a simplistic “non-answer” to your question – sorry – but the truth is that I will stay my course. For me, that is predominately equities and/or cash equivalents, to varying degrees at this time.

There is more going on in Europe (Swiss Franc) but maybe that can wait for later when I have more time.

Best,

Mark

QE in Europe is official now, and at least for now I notice the 10 yr is stable, maybe going up in interest rate a bit ...

one comment I noticed was that the European central banks, doing QE, were buying bonds "including government debt", that latter which I had thought maybe the Fed had done, but maybe not ... that's pure old 'printing money' sure enough

Quote: RaleighCrapsI am trying to figure out ways to preserve my IRA (401K) accounts given the current markets.

YES, I do know that trying to time the markets is not a recommended play, and many who try it, don't fare as well as they could have otherwise.

But I just can't see where investing new money in stocks right now is going to work out in the short term. We have been on a 7 year bull run, yet our economy seems as stagnant now as it was 5 years ago. Layoffs are as common now as then. Even though the jobless numbers appear to have gone down, I'm not sure they are accurately accounting for the many people who have been out of work so long they have given up even looking. Many of the pundits I read are saying a pull back is inevitable, although some of them were saying that last year, and that was not a pull back by any means..... The global economy is more tightly coupled now, than it was in years past, so the old play of US market down, foreign markets up, is not really available any longer.

The bond market does not look very attractive, with interest rates so low, the bond values are going to get killed as interest rates rise, which they have to do pretty soon.

So as I see it, equities are not safe, world markets are not safe, and bonds are not a good play. Real estate has been on a tear, so that will likely pull back as well, if the markets start to tumble. Energy used to be a nice place to hide, but since oil started this free fall, and the Saudi saying oil will never go back to $100 a barrel, what will happen in the energy sector? Natural gas supplies are going to be saturated when Marcellus Shale reserves come on-line.

So what are your thoughts for investing? What to do?

There is to much creative accounting going on in the goverment over the unemployment numbers. I prefer using simple numbers. So 92,000,000 americans are unemployed.

92,000,000/330,000,000 = an unemployment rate of 28%.

The 10th Man

" If you want to know where the next bear market is, look around at the people who are enjoying unimaginable wealth. Mr. Market has a habit of correcting things over time.

My guess is that you won’t be paid $200K/year to drive trucks in North Dakota for much longer. The best thing about capitalism is that everything is temporary. The last time around, people had the stock, could have sold it, and didn’t.

It will be the same this time. They will ride it all the way to the bottom. It’s human nature. Everyone gives the GoPro guy so much crap for stuffing everyone with stock, but maybe he knows something the rest of us don’t."

Best,

Mark

So this week, nearly one year later, my tenants made an offer to buy the property, which I have accepted (settlement next month). I was a little surprised they were doing well enough and had secured financing to be able to be in this position. Good for them. The sale price and profit isn't what I envisioned when I purchased the property, but I am making a little profit. So the experience didn't work out as planned, but after costs and including the rent I have received for the last 11 months, I am profiting just over 9% of purchase price.

Now to figure out what to do and where to park that portion of my bankroll, where it will be safe and I can generate a little money from it.

My brother in law went to ND to drive truck when they were desperate fow workers and housing was cheap he was making 75k a year. He bought his own truck and after expenses hes making 150k a year. He was thinking of buying a 2nd truck and splitting the profit with his son. Not now, Apparently its horrible now, everybody is getting laid off.Quote: Dicenor33Truck drivers in North Dakota are making 200k? Well, most owners operators are making 150~200k. The question is, what's left to the driver? Equipment alone cost 200k, fuel, tolls, insurance, taxes. 37k no matter how you cut it.

Prepare to be petrified: I was laid off today. :(Quote: odiousgambitI'm scared to ask if all of our members employed-by-oil [so to speak] are all still fully employed

Quote: teddysPrepare to be petrified: I was laid off today. :(Quote: odiousgambitI'm scared to ask if all of our members employed-by-oil [so to speak] are all still fully employed

Well, crud.

Sorry, teddy!

Guessing, though, you're pretty employable with the law degree. Hope you find better work soon.

Quote: odiousgambitI'm scared to ask if all of our members employed-by-oil [so to speak] are all still fully employed

One of my paychecks comes from an oil company although my employment is from a division that has nothing to do with oil.

25% invested in individual stocks (currently all of it is invested in KNX)

The remaining money is invested in low cost index funds:

30% domestic equity

15% foreign developed equity

10% emerging markets

15% real estate

7.5% short term US treasury bonds

7.5% intermediate term US treasury bonds

15% treasury inflation protected securities (TIPS)

In the past I took much more risk- up to 60% of my money was invested in 2 stocks (FDS, KNX). The added risk netted substantial gains, so I sold all of FDS, half of KNX, and diversified.

Quote: HowManyThe added risk netted substantial gains, so I sold all of FDS, half of KNX, and diversified.

Nice move. I haven't had all my money in one or two stocks since having any at all came from my employer's stock purchase plan; I'd suggest never doing that again, nice it worked out though.

Here's an article that talks about how you would fare if you were in cash during bear markets.........

"The stock market has a tendency to move in six-to-eight year cycles. The current bull market is now at seven years and there are several indicators signaling weakness. A bear market could be about to emerge. Beyond market cycles and technical indicators, rising interest rates can cause weakness in the equities market."

.

.

.

"The chart below shows the gain you would have from 1995 to 2015 if you sold your stock holdings when the U.S. stock market topped, avoiding the last two bear markets.

Having a 100% cash position during bear markets would have generated 635% return on investment, which is a 31% average annual return. The numbers are staggering to say the least. "

Quote: RaleighCrapsHere's an article that talks about how you would fare if you were in cash during bear markets.........

This has been well known for a long time. If you could do this perfectly very well at all you wouldn't have to worry about picking the right stocks or anything. It's maddening to think about since it would pay off if you could just improve your results some by being able to do it right once in a while. That means timing it correctly *twice* however.

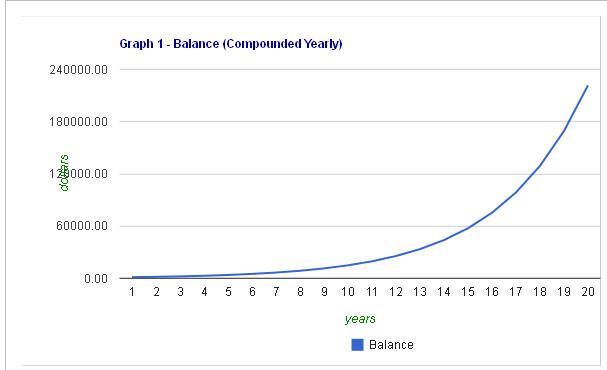

So well known I thought I could find more than I did with google. I have seen a demonstration of the potential of timing on every possible opportunity and it is just awesome [couldn’t find anything just now]. I don’t doubt the figure they use, 31%, is stating it conservatively.

Here is a chart showing someone’s results starting with $1000 over 20 years [and no further investment] getting 31% increases annually. I used http://www.thecalculatorsite.com/finance/calculators/compoundinterestcalculator.php

That’s turned into over $221,000.

So, what are we waiting for? The market is overdue for a correction, right?

Unfortunately, nobody can do this. The market is already reflecting all known factors as is - imperfectly of course - but good enough to foil this practice. Again, this is well known, but people who have tried this have been followed. Sometimes they get the exit time correctly, but, being worry warts, they stay out and do not get back in at the right time. You have to be right on the timing twice! Cash is no safe place to be! To get something out of this post, please at least absorb this fact! Cash is no safe place to be!

Being a gambler, I can’t resist market timing. But what I do is two things:

*I rebalance my holdings maybe once a year. This is similar to market timing but actually gets the blessing of all the more informed gurus out there.

*When it is time to rebalance by buying stocks, I do try to time this. I feel like I do OK by waiting for swoons, but it probably can be shown that I have wasted my efforts [I don’t know].

It’s probably fair to say I wander into more market timing efforts than purely the above, just to make it clear I am not a Saint.

There are plenty of investment outfits who claim they can do market timing. To me, this just underlines the danger of this kind of thinking. It is true temptation.

One final thing: the same financial advisors who like to tell you not to do market timing also like to say that the average investor is terrible at it. The more instinctive your approach is, the more likely you are to get the stink-eye about this. So here is a meme:

As an investor I wanted to be a better Market Timer.

So I quit being an Average Investor.

Quote: RaleighCrapshttp://www.msn.com/en-us/money/markets/will-the-stock-market-correct-or-completely-collapse-in-2015/ar-AAammWY

Here's an article that talks about how you would fare if you were in cash during bear markets.........

Raleigh and Odious -

Two excellent posts, once again. I began following this thread not long ago but it has my complete attention. Sometimes I can gauge add'l insights from forums NOT related to markets and finance.

Many will say that it is folly to try to time markets with entries and exits. I disagree. It's true that no one can pick exact tops and bottoms 100 percent of the time, but that is not the goal. The goal should be capital preservation. Period.

How? Risk management. There are useful tools available to determine when risk is high (bad time to enter) and when it's low (good). I've hinted in a few posts at some that I use. Yes (to those who will scoff), they are charts depicting price and breadth as well as sentiment.

Personally, and with three decades experience on the other side of the desk, I am glad I got that religion. It protected clients from Q2, 2000 through Q3, 2002 as well as 2008 and 2009. By Q1, 2003, my moneyline (aggregate of total account values) was making NEW money by having avoided the sharp losses most experienced. Same is true for the second shoe that dropped. 2010 started seeing profitability again. Some people too ten years to break even. Some never did at all.

A guy by the name of Sosnowy wrote a book about "timing" in the mid 90's. To paraphrase, (my words) "The key to investment success is AVOIDING severe losses."

I have no problem at all being only 30-40% invested right now because, even though the cash equivalents are earning less than zero, I work best at puting that cash back to work when indicators I trust demonstrate that risk is low. That's also when I am the most scared to act, but act I do - typically with both fists loading the truck up.

It works.

I don't outstrip market results, I simply get similar results (often better) with far less risk, volatility and drawdowns.

I may pass through again this weekend to add a couple more (opinionated) thoughts.

Best,

Mark

Quote: mdhovlandI may pass through again this weekend to add a couple more (opinionated) thoughts.

Your input is appreciated.

Like a Craps player who doesn't seem to realize that if the game goes slower, this is better for him, the market being closed is a downer for me LOL. I should realize that daily attention is not needed.

Do you also find that these little dips we get are unplayable? The Dow going down 300 points doesnt mean what it used to mean [not even 2%]. I know what I want to do with 10% corrections, but 300 points down one day, then back up the same amount the next does nothing but irritate me.

Obviously most stocks tend to do poorly in a bear market and there are times to hold a lot of cash and just wait. But I don't think that strategy works as well going in and out of funds & indexes. Too much data on the reduction in returns if you miss the 10 best up days in a market, etc..

Find 15-20 good companies with solid prospects for growth and buy them at good valuations and/or on breakouts on good volume days when you know the markets are not in a general downtrend (e.g. it is getting scarier to do that know vs. a year ago).

Despite the bubble talk there are still good values out there on quality growth companies that I have very little doubt will do very well over the next 5 years.

Quote: mdhovlandA guy by the name of Sosnowy wrote a book about "timing" in the mid 90's. To paraphrase, (my words) "The key to investment success is AVOIDING severe losses."

let us know if you see a crash coming so we can sell into Bonds :)

Quote: odiousgambitI can see a crash coming ... in bonds!

oh wow.. stocks AND bonds crashing at the same time.

*mind explodes*

how does one mitigate this?

Quote: 100xOddsQuote: odiousgambitI can see a crash coming ... in bonds!

oh wow.. stocks AND bonds crashing at the same time.

*mind explodes*

how does one mitigate this?

Cash is king, at least for a short time frame. I'm also betting on a run back to precious metals.

Quote: 100xOddsQuote: odiousgambitI can see a crash coming ... in bonds!

oh wow.. stocks AND bonds crashing at the same time.

*mind explodes*

how does one mitigate this?

No-load munis? IDK, for sure. Mine is tucked away for the long run.

Quote: odiousgambit

...

Do you also find that these little dips we get are unplayable? The Dow going down 300 points doesnt mean what it used to mean [not even 2%]. I know what I want to do with 10% corrections, but 300 points down one day, then back up the same amount the next does nothing but irritate me.

Odious - I understand what you mean. In percentage terms, while now more volatile than in times past and the moves also being a slight bit greater in magnitude, it is still a simply a relative move. But, the nominal moves can cause concern for some. We either accept or decline that part of it.

An employee/plan participant exclaims:

"I lost $10,000 in my 401(k) last month!"

A fellow asks back, "Really - what is your account balance?"

"It WAS $400,000 - I don't think I can take this any longer!"

(The guy that asked the balance walks away muttering and shaking his head... with the tune "Compared to What" crashing into his head... ...)

Les McCann and Eddie Harris - Compared to What

To your question, I don't find these dips unplayable at all if that's the trading program one want's to use.

They are very suitable for swing-trading (example given - $50K or more to be used to trade 5-7 names) over the course of a few days to a few weeks. There are some money management rules that must be adhered to, however, for position sizing, Reward-to-Risk ratios, etc. It can be a decent mechanical method to achieve solid monthly returns of 2-3% or more. It takes a lot of (effort and) mental discipline PLUS a solid methodology.

There are several technical indicators which can identify short-term overbought/oversold conditions points of entry. (For the SPX, I count 4 solid entry points since the beginning of November, 2014 - 5 if you count the October low - using a couple simple ones.)

Paradigm makes a very valid point in his post. He prefers to find the companies he has confidence in and then evaluate his entry based on price and volume (charts). He is combining both practices, fundamental and technical, and that is a wise approach.

I come at it from the opposite direction, technical then fundamental. I place emphasis on the chart(s) and feel that they lead me to the high quality companies most of the time. I have names which have been owned since 2006 (PG, COST and BEAV), but have taken profits along the way.

Either approach is not infallible, however.

I also agree that a portfolio of a few names (for me, 20-30) is suitable. I prefer a 4% initial position. That’s enough to construct a personal mutual fund.

I find myself between being defined as a position trader and a long term trader. (I like the tax treatment of +12 month holding periods.) I would also return to swing-trading if it suited my time-constrained lifestyle.

Also, and once again -

Most risk in the market is:

50% market

30% sector/group/industry

20% individual stock

RalieghCraps – if you have 8-10 years before the money you are speaking of needs to be used to fund your retirement, you need some equity exposure now to whatever degree you can enable. Even in retirement, you must have some element of it – much more than zero. Plan to draw out ~3.5% annually in retirement from all sources, no more, unless compelled to by RMD's. Ten's of thousand's of Monte Carlo simulations suggest that would fund 30 years of distributions without adverse results.

I'm glad to see this thread getting some traction for you. Even with a dissenting view here and there, it can be useful for potentially anyone who reads it.

Best,

Mark

P.S. - Odious, I'm taking time to follow your chess thread, too. Chess is a game my mentor challenged me to take up 20+ years ago. Now I have - as of the new year. I thought I once played backgammon well. Now I have my doubts!

Quote: 100xOddslet us know if you see a crash coming so we can sell into Bonds :)

I don't know if/when and neither does anyone else - exactly. But you can watch the storm clouds build, then fly around them. Hopefully there's enough fuel on-board to make a safe landing.

I can say that the very first firm I worked for got buried when one of our reps in LA tried to make an interest rate play on Gov't notes and bonds in the 90's (leveraged at 90%+, a huge one I might add). He was wrong, and his clients - not to mention our clients, the remaining 35 of us reps - had to find a new B/D to work through.

I think I linked this elsewhere:

"You know what I worry about? I worry about the baby boomers. I worry about this generation, the worst investors in US history, who got carried out in the tech bear market in 2000 and got caned in the financial crisis of 2008, and after having been hammered twice in the span of 10 years in the stock market, went all-in on bonds.

Why? Bonds are safe. Everyone knows stocks are not safe.

Now, in retirement, none of these people expect their bond mutual funds to get cut in half, which would happen if interest rates went up about 3%-5%.

Imagine if they did!"

The Crazy Man’s Guide to the Bond Market

It's also argued that the recent change in the language from the FOMC gives them (the FOMC) an excuse not to raise rates. The FED wrote in it's notes:

"It will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term."

Please understand - that is not my work or observation, but I don't disagree either. It's apparent they replaced the word "patient" with the words "reasonably confident", still suggesting uncertainty. So, probably not this year and not likely in an election year (2016).

You can clearly see why these markets get foiled up by "financial engineering", right?

The FED will get concerned when inflation trends toward and/or exceeds 2%. Reported inflation is currently at ~1.3% and has ranged from 1 to 2% since 2010. It's present trend is aiming back toward 1%. It would seem that right now the FED has no intention of a rate hike no matter how they package their remarks. I have nothing more to add - there's not much more to be said.

(THIS ^^^^ is exactly why I try to avoid the "news." It's also why I try to control what I am able to control.)

Best,

Mark

Quote: rudeboyoiIdk much about stocks. I can imagine there's prob a lot of system peddlers out there though.

link to original post

Earlier today I stumbled on something called the Halloween Strategy:

Quote: InvestopediaThe Halloween strategy, Halloween effect, or Halloween indicator, is a market-timing strategy based on the hypothesis that stocks perform better between Oct. 31 (Halloween) and May 1 than they do between the beginning of May through the end of October. The strategy posits that it is prudent to buy stocks in November, hold them through the winter months, then sell in April, while investing in other asset classes from May through October. Some who subscribe to this tactic say not to invest at all during the summer months.

This dates back to the 16th Century and the first London stock market. Sounds about as sensible as other ideas from that time period (e.g., blood letting) but apparently some modern studies show that it appears to pay off even if nobody knows why. Maybe I'll stick some spare cash into a general market ETF and see what happens between now and May.

Quote: vegasMaxxx...I see you reply to a ton of posts but you really don't say much. Why are you in such a hurry to get your post count up?

link to original post

I think that he's reached the requisite threshold and look forward to visiting his preferred website $;o)

for a market such as the U.S. stock market which has a proven long term upward bias I believe there is not a codified strategy that can beat the simple strategy of buy and hold - referring to index or mutual funds which cover the broad market

a relatively small number of talented individuals can and do beat the market

but they do this with knowledge and insight that few others have

they don't do it because they have a codified strategy that follows rules of when to buy and sell

.

I disagree. Well, depends on what you mean by codified strategy.Quote: lilredrooster___________

for a market such as the U.S. stock market which has a proven long term upward bias I believe there is not a codified strategy that can beat the simple strategy of buy and hold - referring to index or mutual funds which cover the broad market

a relatively small number of talented individuals can and do beat the market

but they do this with knowledge and insight that few others have

they don't do it because they have a codified strategy that follows rules of when to buy and sell

.

link to original post

Within any such mainstream market, there will be sectors that have disparate and longstanding trends. An investor only needs to click on the right sector at the right time and find himself swept forward faster and higher than the entire market. E.g. realise that online shopping or electric vehicles are a hot trend, and away he goes till the trend turns. Because sectors are huge, they can be slow enough to turn up or down that an aware investor can jump to the next sector in a timely manner.

Or even leap between markets entirely, such as moving funds to India, Asia, Russia, South America, Europe.

Of course, all sectors and markets can turn down separately or in unison in the blink of an eye or upon a major world event. March 2020 blipped many a chart.

Quote: OnceDearI disagree. Well, depends on what you mean by codified strategy.Quote: lilredrooster___________

for a market such as the U.S. stock market which has a proven long term upward bias I believe there is not a codified strategy that can beat the simple strategy of buy and hold - referring to index or mutual funds which cover the broad market

a relatively small number of talented individuals can and do beat the market

but they do this with knowledge and insight that few others have

they don't do it because they have a codified strategy that follows rules of when to buy and sell

.

link to original post

Within any such mainstream market, there will be sectors that have disparate and longstanding trends. An investor only needs to click on the right sector 𝙖𝙩 𝙩𝙝𝙚 𝙧𝙞𝙜𝙝𝙩 𝙩𝙞𝙢𝙚 and find himself swept forward faster and higher than the entire market. E.g. realise that online shopping or electric vehicles are a hot trend, and away he goes till the trend turns. Because sectors are huge, they can be slow enough to turn up or down that an aware investor can jump to the next sector 𝙞𝙣 𝙖 𝙩𝙞𝙢𝙚𝙡𝙮 𝙢𝙖𝙣𝙣𝙚𝙧.

Or even leap between markets entirely, such as moving funds to India, Asia, Russia, South America, Europe.

Of course, all sectors and markets can turn down separately or in unison in the blink of an eye or upon a major world event. March 2020 blipped many a chart.

link to original post

I disagree with your disagreement

you're talking about 𝙩𝙞𝙢𝙞𝙣𝙜 𝙩𝙝𝙚 𝙢𝙖𝙧𝙠𝙚𝙩..................something much easier said than done

also, you're not referring to a codified strategy which is what I was referring to

yes, there are some, I believe few, who can do this or something similar - but it's not codified - it requires knowledge and insightful speculation

also, and very important..................the buy and holder is subject to only nominal capital gains taxes each year

those who trade actively - if they have a yearly profit - will have capital gains tax obligations - often significant - each and every profitable year - at least if they are based in the U.S.

also, something I have personal experience with...............if part of the reason a person is investing is to pass on wealth to his heirs.....................when the funds are passed on due to a death - all of the accumulated capital gains are forgiven - for the beneficiary - they have no capital gains tax obligation - due to something that accountants call 𝙨𝙩𝙚𝙥 𝙪𝙥 𝙗𝙖𝙨𝙞𝙨

if a person is trading in an IRA account then they are not subject to capital gains taxes and the above points do not apply

.

I accept and agree with your comment about codified strategy. Timing market sectors does require insight or luck.Quote: lilredroosterQuote: OnceDearI disagree. Well, depends on what you mean by codified strategy.Quote: lilredrooster___________

for a market such as the U.S. stock market which has a proven long term upward bias I believe there is not a codified strategy that can beat the simple strategy of buy and hold - referring to index or mutual funds which cover the broad market

a relatively small number of talented individuals can and do beat the market

but they do this with knowledge and insight that few others have

they don't do it because they have a codified strategy that follows rules of when to buy and sell

.

link to original post

Within any such mainstream market, there will be sectors that have disparate and longstanding trends. An investor only needs to click on the right sector 𝙖𝙩 𝙩𝙝𝙚 𝙧𝙞𝙜𝙝𝙩 𝙩𝙞𝙢𝙚 and find himself swept forward faster and higher than the entire market. E.g. realise that online shopping or electric vehicles are a hot trend, and away he goes till the trend turns. Because sectors are huge, they can be slow enough to turn up or down that an aware investor can jump to the next sector 𝙞𝙣 𝙖 𝙩𝙞𝙢𝙚𝙡𝙮 𝙢𝙖𝙣𝙣𝙚𝙧.

Or even leap between markets entirely, such as moving funds to India, Asia, Russia, South America, Europe.

Of course, all sectors and markets can turn down separately or in unison in the blink of an eye or upon a major world event. March 2020 blipped many a chart.

link to original post

I disagree with your disagreement

you're talking about 𝙩𝙞𝙢𝙞𝙣𝙜 𝙩𝙝𝙚 𝙢𝙖𝙧𝙠𝙚𝙩..................something much easier said than done

also, you're not referring to a codified strategy which is what I was referring to

yes, there are some, I believe few, who can do this or something similar - but it's not codified - it requires knowledge and insightful speculation

also, and very important..................the buy and holder is subject to only nominal capital gains taxes each year

those who trade actively - if they have a yearly profit - will have capital gains tax obligations - often significant - each and every profitable year - at least if they are based in the U.S.

also, something I have personal experience with...............if part of the reason a person is investing is to pass on wealth to his heirs.....................when the funds are passed on due to a death - all of the accumulated capital gains are forgiven - for the beneficiary - they have no capital gains tax obligation - due to something that accountants call 𝙨𝙩𝙚𝙥 𝙪𝙥 𝙗𝙖𝙨𝙞𝙨

.

link to original post

Capital Gains tax rules vary by nation. Here in the UK we can have certain accounts where No CGT obligation accrues, But I don't think we escape CGT on death as our inheritance taxes are not so easy going.

Quote: lilredroosterQuote: OnceDearI disagree. Well, depends on what you mean by codified strategy.Quote: lilredrooster___________

for a market such as the U.S. stock market which has a proven long term upward bias I believe there is not a codified strategy that can beat the simple strategy of buy and hold - referring to index or mutual funds which cover the broad market

a relatively small number of talented individuals can and do beat the market

but they do this with knowledge and insight that few others have

they don't do it because they have a codified strategy that follows rules of when to buy and sell

.

link to original post

Within any such mainstream market, there will be sectors that have disparate and longstanding trends. An investor only needs to click on the right sector 𝙖𝙩 𝙩𝙝𝙚 𝙧𝙞𝙜𝙝𝙩 𝙩𝙞𝙢𝙚 and find himself swept forward faster and higher than the entire market. E.g. realise that online shopping or electric vehicles are a hot trend, and away he goes till the trend turns. Because sectors are huge, they can be slow enough to turn up or down that an aware investor can jump to the next sector 𝙞𝙣 𝙖 𝙩𝙞𝙢𝙚𝙡𝙮 𝙢𝙖𝙣𝙣𝙚𝙧.

Or even leap between markets entirely, such as moving funds to India, Asia, Russia, South America, Europe.

Of course, all sectors and markets can turn down separately or in unison in the blink of an eye or upon a major world event. March 2020 blipped many a chart.

link to original post

I disagree with your disagreement

you're talking about 𝙩𝙞𝙢𝙞𝙣𝙜 𝙩𝙝𝙚 𝙢𝙖𝙧𝙠𝙚𝙩..................something much easier said than done

also, you're not referring to a codified strategy which is what I was referring to

yes, there are some, I believe few, who can do this or something similar - but it's not codified - it requires knowledge and insightful speculation

also, and very important..................the buy and holder is subject to only nominal capital gains taxes each year

those who trade actively - if they have a yearly profit - will have capital gains tax obligations - often significant - each and every profitable year - at least if they are based in the U.S.

also, something I have personal experience with...............if part of the reason a person is investing is to pass on wealth to his heirs.....................when the funds are passed on due to a death - all of the accumulated capital gains are forgiven - for the beneficiary - they have no capital gains tax obligation - due to something that accountants call 𝙨𝙩𝙚𝙥 𝙪𝙥 𝙗𝙖𝙨𝙞𝙨

if a person is trading in an IRA account then they are not subject to capital gains taxes and the above points do not apply

.

link to original post

Short term capital gains are a killer for active traders. Worse than the vig. My guess is less than 5% sitting in their pajamas, actively trading, are actually making money YOY.

Up to 37% for capital gains means you’ve got a LOT to overcome.

No capital gains, no income tax. It is better than a Defined Plan or Sliced Beer.

Quote: billryanI-B-D-S.

No capital gains, no income tax. It is better than a Defined Plan or Sliced Beer.

link to original post

Otherwise known as Irritable Bowel Disease.

I believe this may be the first whiff of a long overdue correction. Stock market capitalization currently stands at about 200% of GDP, the highest ever. In 2000 it peaked at 140% right before the tech bubble burst

The market will revert back to a normal valuation (80 - 100% of GDP). Always does…question is when not if. I have trailing stop loss orders on everything

Real estate bubble to burst right after stocks.

It’s unfortunate that the USA is now a boom and bust economy. Crashes about every ten years like a developing nation. As usual, the Fed is mostly to blame…they left interest rates way too low for way too long…again