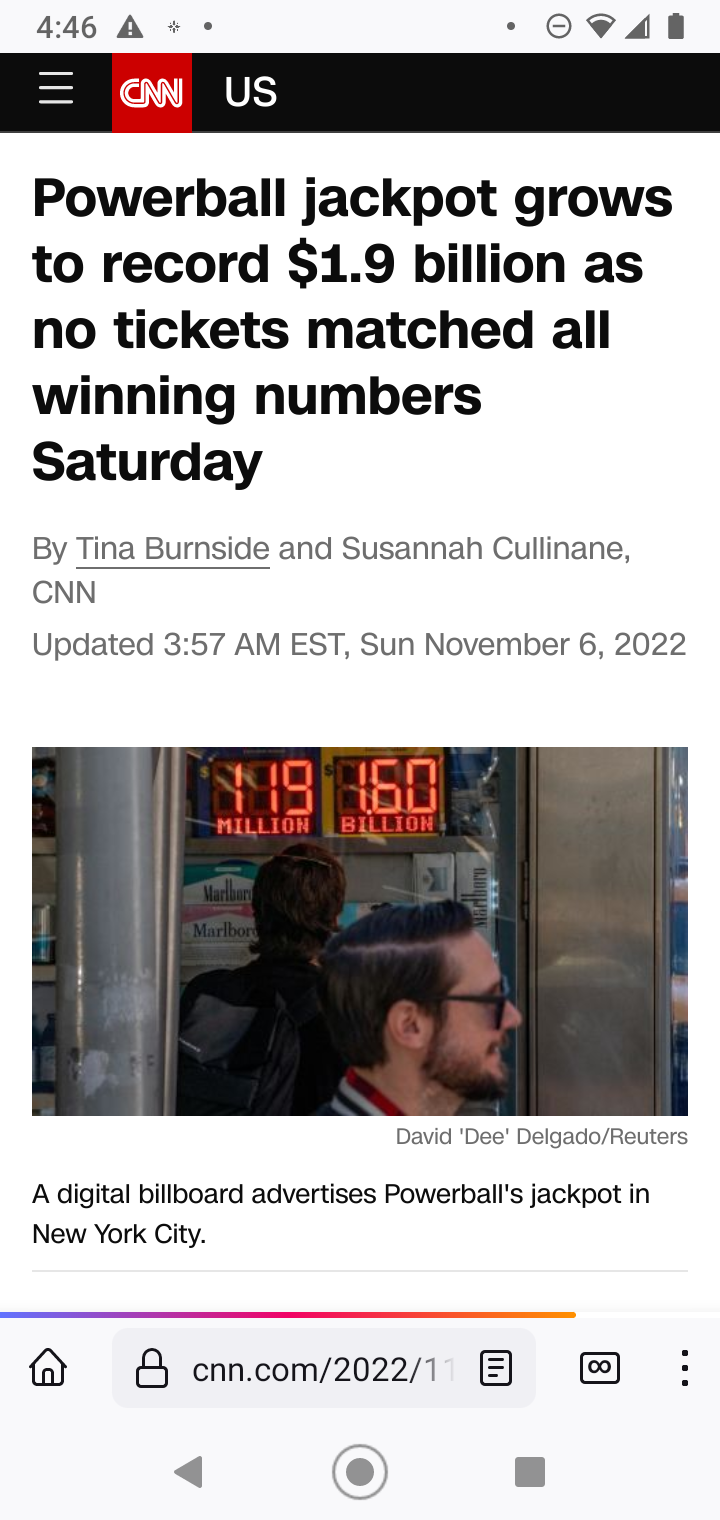

Powerball hits $1 Billion

Quote: tuttigymQuote: GenoDRPhQuote: tuttigymQuote: rsactuaryI guess, yes, a slight advantage? Because if you cashed both in the same year, the entire second ticket would be taxed at the highest bracket, whereas if you waited a small portion of it would be taxed at the lower levels.

However, you could invest it in T-bills and earn more interest than you would get with the tax break pretty quickly, I would think.

link to original post

Let's see, you win say $600 million take home and you are looking to invest is some interest-bearing vehicle? Why, to pay more taxes or increase the size of your estate? You do realize that if one does not spend it all somehow, the IRS will tax your remainder estate through the federal estate tax laws. That tax rate starts at 55%, I believe.

tuttigym

link to original post

Federal Estate Taxes no where near 55%: https://www.investopedia.com/estate-tax-exemption-2021-definition-5114715

That's why it's important to have a trust or trusts claim the prize and handle the money year over year. Lots of tax benefits to that, as well as anonymity.

Gene

link to original post

Gene, The first $12+ mil is exempt after which anything over $1 mil is taxed at 40% federally, but there can be state estate taxes on top.

Your take on trusts is not accurate. What you are thinking about is a foundation. Trusts, i.e., living revocable type, are a means to transfer assets in an estate or entity directly without a court intervening. If there are stand-alone trusts that invest and make money, they must file tax returns just like an individual or business.

That is why one must, IMO, have a personal A B living trust to avoid probate and transfer assets to heirs in a really short period of time.

tuttigym

link to original post

Lots of people claim lottery prizes in the name of a trust. Happens all the time. Keeps the winners name from being public. can be used a workaround from the IRS gift maximum, and lots of other benefits both financial and practical. Lottery winnings in the name of trust also avoid any estate taxes. There are other types of trusts than a living revocable trust. Talk to any lawyer and they'll confirm what I said.

Gene

Quote: GenoDRPh

Lots of people claim lottery prizes in the name of a trust. Happens all the time. Keeps the winners name from being public. can be used a workaround from the IRS gift maximum, and lots of other benefits both financial and practical. Lottery winnings in the name of trust also avoid any estate taxes. There are other types of trusts than a living revocable trust. Talk to any lawyer and they'll confirm what I said.

Anominity using a trust to collect is correct. A trust gifting to individuals is NOT tax free. If the gift exceeds the federal maximum, it is taxed to the recipient. Dispursement of trust assets will be taxed to recipients with the exception of charities. If one is a beneficiary of money from a trust, it can be treated as a gift or income tax by the IRS. They will get their "pound of flesh." As I stated before, if the trust invests and makes money, the first trustee or named administrator must file a tax return.

tuttigym

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

Quote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

Quote: GenoDRPhQuote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

link to original post

Why waste money on attorneys and accountants with their fancy schooling and book learning when you can get free advice on the internet?

Quote: billryanQuote: GenoDRPhQuote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

link to original post

Why waste money on attorneys and accountants with their fancy schooling and book learning when you can get free advice on the internet?

link to original post

Not only that, it's all true! They can't put it on the internet if it isn't true!

Quote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

Quote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

It depends on how comfortable you need to live. My sister just retired on Long Island and is feeling the pinch. Maybe she doesn't need the country club and the beach house. Maybe play two rounds a week instead of five.

Starting Monday, I'm RV'ing fulltime and am the happiest I've been in the last couple of years. Call me crazy, but I'd rather watch a lightning storm over the Mule Mountains than see another Cirque show.

Quote: billryanQuote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

It depends on how comfortable you need to live. My sister just retired on Long Island and is feeling the pinch. Maybe she doesn't need the country club and the beach house. Maybe play two rounds a week instead of five.

Starting Monday, I'm RV'ing fulltime and am the happiest I've been in the last couple of years. Call me crazy, but I'd rather watch a lightning storm over the Mule Mountains than see another Cirque show.

link to original post

Congrats on joining terapined. Don�t you have tons of collectibles? Going in a storage thingie?

Quote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I agree, $1mm is not "instant retirement money," but it is a sizeable chunk that would supplement my current standard of living quite nicely and set me up for a decent retirement eventually.

I could retire on $2mm and live quite comfortably, $3mm or more and I'd definitely be making some upgrades.

Quote: GenoDRPhQuote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

link to original post

After you linked me to the info, I am now re-educated on the federal estate tax rate. My info was old and the rates have been revised since then (over 30 yrs.). I do not disagree that expert legal advice is required to navigate those financial waters. My point regarding the estate tax is that at some point, if someone in your family has assets that exceed that $12+ million threshold, the estate tax will come into play if not, the income tax will be involved. For example, if your trust pays your child, after you are deceased, $150 mil, that beneficiary gets nailed for fed and state income taxes or even estate taxes because the beneficiary is required to file an IRS 706 form, so yes, the trust does not pay estate taxes but the beneficiaries will be taxed in some way big time. As I stated, the IRS will get theirs.

BTW most of my eligible assets are currently in a trust. I still pay taxes; my trust does not; when I die, the assets will transfer seamlessly without probate, court intervention, and estate tax free (below the threshold), but my beneficiaries might have to pay income taxes because of the type of assets being inherited.

tuttigym

Quote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I have been retired for over 20 years. I am debt free and live a very comfortable life. I deny myself nothing, and my total annual expenditures rarely exceed $50k including, taxes, insurance, and gifting. But that is just me.

tuttigym

Agree with Tuttigym. As long as you are completely debt free and healthy, you can live quite comfortably on $4k per month.Quote: tuttigymQuote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I have been retired for over 20 years. I am debt free and live a very comfortable life. I deny myself nothing, and my total annual expenditures rarely exceed $50k including, taxes, insurance, and gifting. But that is just me.

tuttigym

link to original post

However, if you are like most Americans with a big a$$ mortgage payment, financed expensive cars etc then you need a lot more than $4k just to cover debt payments, let alone pay for current expenses and save for the future

Quote: tuttigymQuote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I have been retired for over 20 years. I am debt free and live a very comfortable life. I deny myself nothing, and my total annual expenditures rarely exceed $50k including, taxes, insurance, and gifting. But that is just me.

tuttigym

link to original post

That is awesome and I am happy for you. To me retirement would include about 25% of my time travelling and staying in 4 star hotels and eating at 4 star restaurants. I am guessing that alone would cost around $300 a day. Other than that I assume my biggest cost will be medical insurance which I guess will be near $2000 a month for the wife and I.

I think the standard is expect to spend about 4% of your retirement per year. If that is "typical" I would want at least $3 million in the bank. Obviously it is different if you have money coming in from a pension which I won't. I expect my Social Security will cover my health insurance costs in six years when I turn 62. Until that time I will not have any income coming in and I will have to live out of my investments.

Quote: Ace2Agree with Tuttigym. As long as you are completely debt free and healthy, you can live quite comfortably on $4k per month.Quote: tuttigymQuote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I have been retired for over 20 years. I am debt free and live a very comfortable life. I deny myself nothing, and my total annual expenditures rarely exceed $50k including, taxes, insurance, and gifting. But that is just me.

tuttigym

link to original post

However, if you are like most Americans with a big a$$ mortgage payment, financed expensive cars etc then you need a lot more than $4k just to cover debt payments, let alone pay for current expenses and save for the future

link to original post

Hopefully, by the time you retire, the big mortgage and expensive cars are paid off. If not,that was either poor planning or a good plan executed poorly.

Gene

Quote: DRichQuote: tuttigymQuote: DRichQuote: TigerWu

Hitting five numbers, minus the Powerball, is worth a million. That would be plenty for me.

I don't know your age or situation, but for me $1 million dollars would not be nearly enough for me to retire. With $2 million I might be able to retire but I would not be able to do much more than survive. My Number today is $3.5 million to retire comfortably.

link to original post

I have been retired for over 20 years. I am debt free and live a very comfortable life. I deny myself nothing, and my total annual expenditures rarely exceed $50k including, taxes, insurance, and gifting. But that is just me.

tuttigym

link to original post

That is awesome and I am happy for you. To me retirement would include about 25% of my time travelling and staying in 4 star hotels and eating at 4 star restaurants. I am guessing that alone would cost around $300 a day. Other than that I assume my biggest cost will be medical insurance which I guess will be near $2000 a month for the wife and I.

I think the standard is expect to spend about 4% of your retirement per year. If that is "typical" I would want at least $3 million in the bank. Obviously it is different if you have money coming in from a pension which I won't. I expect my Social Security will cover my health insurance costs in six years when I turn 62. Until that time I will not have any income coming in and I will have to live out of my investments.

link to original post

Why did you make those investments, if not to be able to enjoy them? Show me your million, and I'll show you how to get 8% off of it.

I can live nicely off my dividends, but that's because I don't have half my assets tied up in a non-income-producing sinkhole like a house. I'm two years into collecting my early SS and have not spent a dime of it. It's all gone into IBonds or will, in January.

There are other ways to go about things.

If I live to be 90, I imagine I'll pretty much run out of money and be stuck living off SS, but I'd guess there is about 5% or less chance of that. One male in my rather large family has celebrated his 82nd birthday and only one other lived to be 75. I suspect I'll honor my family tradition. My Dad died at 53 and his only brother to survive their youth died at 61. Not much better on my mom's side, either. Four of the six males died in the fifties and sixties. The women tend to live longer.

Quote: tuttigymQuote: GenoDRPhQuote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

link to original post

After you linked me to the info, I am now re-educated on the federal estate tax rate. My info was old and the rates have been revised since then (over 30 yrs.). I do not disagree that expert legal advice is required to navigate those financial waters. My point regarding the estate tax is that at some point, if someone in your family has assets that exceed that $12+ million threshold, the estate tax will come into play if not, the income tax will be involved. For example, if your trust pays your child, after you are deceased, $150 mil, that beneficiary gets nailed for fed and state income taxes or even estate taxes because the beneficiary is required to file an IRS 706 form, so yes, the trust does not pay estate taxes but the beneficiaries will be taxed in some way big time. As I stated, the IRS will get theirs.

BTW most of my eligible assets are currently in a trust. I still pay taxes; my trust does not; when I die, the assets will transfer seamlessly without probate, court intervention, and estate tax free (below the threshold), but my beneficiaries might have to pay income taxes because of the type of assets being inherited.

tuttigym

link to original post

Estate tax over $12 mill or whatever? Simple solution. By the time I die, my estate won't be worth over $12 million. By then I would have given away or spent down to be below that threshold.

Gene

Quote: billryan[

Why did you make those investments, if not to be able to enjoy them? Show me your million, and I'll show you how to get 8% off of it.

The only money I have making 8% is my I-Bonds and that is going down below 7% shortly. The majority of my investments are down this year.

Quote: GenoDRPhQuote: tuttigymQuote: GenoDRPhQuote: tuttigymGene: Suppose you win a lottery jackpot and collect in the name of a trust. The amount is $250 mil. Now you want your child to receive $5 mil from the trust which exceeds the federal personal lifetime gifting amount of $1,000,000.

Do you not think that the IRS will tax that gift? There are rules which must be followed, and the IRS rules.

tuttigym

link to original post

You're changing the goalposts, amigo. The question presented was the estate tax, which is no where near starting at 55%, as you claim. Gift taxes and income taxes are a different topic.

I am not collecting the jackpot in the name of the trust. The trust is the bearer of the ticket, as the ticket is a bearer instrument. How am I getting my money? Am I a named beneficiary of the trust? How is my kid getting the money I am giving to them? Are they named beneficiaries of the trust, or am I writing $1 million checks from my personal bank account to them? Do I not think the IRS will tax that gift? I think, and this is the best answer I am going to give, I would seek out and follow expert legal, financial and accounting advice as to the best methods to do what I want to do with my new-found-wealth.

link to original post

After you linked me to the info, I am now re-educated on the federal estate tax rate. My info was old and the rates have been revised since then (over 30 yrs.). I do not disagree that expert legal advice is required to navigate those financial waters. My point regarding the estate tax is that at some point, if someone in your family has assets that exceed that $12+ million threshold, the estate tax will come into play if not, the income tax will be involved. For example, if your trust pays your child, after you are deceased, $150 mil, that beneficiary gets nailed for fed and state income taxes or even estate taxes because the beneficiary is required to file an IRS 706 form, so yes, the trust does not pay estate taxes but the beneficiaries will be taxed in some way big time. As I stated, the IRS will get theirs.

BTW most of my eligible assets are currently in a trust. I still pay taxes; my trust does not; when I die, the assets will transfer seamlessly without probate, court intervention, and estate tax free (below the threshold), but my beneficiaries might have to pay income taxes because of the type of assets being inherited.

tuttigym

link to original post

Estate tax over $12 mill or whatever? Simple solution. By the time I die, my estate won't be worth over $12 million. By then I would have given away or spent down to be below that threshold.

Gene

link to original post

That is a great plan. Does that include the mythical $250 mil lotto winnings or just your current assets?

tuttigym

You can get insurance for about $100 per month per person. $15k deductible which makes it catastrophic, which is the only kind of insurance you should have for anything IMO. $24k per year for health insurance�I doubt I�ve spent $24k in medical expenses in my entire lifeQuote: DRich[Other than that I assume my biggest cost will be medical insurance which I guess will be near $2000 a month for the wife and I.

I think the standard is expect to spend about 4% of your retirement per year. If that is "typical" I would want at least $3 million in the bank.

link to original post

Forget about �typical�. If you had $3 million in the bank, you�d have earned essentially zero over the past thirteen years. Average market performance is generally only valid for periods over fifty years

Quote: DRichQuote: billryan[

Why did you make those investments, if not to be able to enjoy them? Show me your million, and I'll show you how to get 8% off of it.

The only money I have making 8% is my I-Bonds and that is going down below 7% shortly. The majority of my investments are down this year.

link to original post

Just to finish my current position, I have a six figure income with a less than 4% federal tax burden and no state income tax. My second largest expense is insurance at about $6800/yr which includes medical, auto, and property insurances. My largest expense is gifting. My cash position is enviable and will probably "invest" is CD's as the rates are rising to about 4% which will increase my fed. income taxes some but is a good trade off. Otherwise, I have no need for additional funds as I am now situated.

tuttigym

Quote: DRichQuote: billryan[

Why did you make those investments, if not to be able to enjoy them? Show me your million, and I'll show you how to get 8% off of it.

The only money I have making 8% is my I-Bonds and that is going down below 7% shortly. The majority of my investments are down this year.

link to original post

Two years ago, a friend gave me $25,000 to buy a couple comics or baseball cards that I felt would be a good value. Using his purchase power, I got him six graded comics and four graded baseball cards. The current value is over $60,000. My share of the return- zero. The sports card and comic world exploded during covid and is only now cooling down. I sold everything just after the market peaked but did much better than I dreamed of. All I kept were my baseball cards and toy soldiers.

To put it in perspective- 20,000 comics need about 100 18-inch by 12 by 10 boxes and fills a small bedroom. 20,000 baseball cards fills a 42X36 inch space originally designed for a washer/dryer combo. I did find a box of comics I'd buried away that has a good bit of value to it.

Quote: Ace2You can get insurance for about $100 per month per person. $15k deductible which makes it catastrophic, which is the only kind of insurance you should have for anything IMO. $24k per year for health insurance�I doubt I�ve spent $24k in medical expenses in my entire lifeQuote: DRich[Other than that I assume my biggest cost will be medical insurance which I guess will be near $2000 a month for the wife and I.

I think the standard is expect to spend about 4% of your retirement per year. If that is "typical" I would want at least $3 million in the bank.

link to original post

Forget about �typical�. If you had $3 million in the bank, you�d have earned essentially zero over the past thirteen years. Average market performance is generally only valid for periods over fifty years

link to original post

For me, that does not compute. If one has spent a lifetime working and investing and saving to end up with $3 mil "in the bank." that is NOT "earning ZERO." I am not sure where the 13 years enters the equation.

tuttigym

Interest rates on savings have been essentially zero since 2009.Quote: tuttigym[

For me, that does not compute. If one has spent a lifetime working and investing and saving to end up with $3 mil "in the bank." that is NOT "earning ZERO." I am not sure where the 13 years enters the equation.

tuttigym

link to original post

$3 million �in the bank� times zero equals zero in earnings over that period

Quote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

Comprehension and reading skills are bailing on you Ace. That $6800 INCLUDES medical/health, auto, and homeowners. My property taxes were just $1200 this year too. I know you can do better. Just try a little harder.

tuttigym

Quote: Ace2Interest rates on savings have been essentially zero since 2009.Quote: tuttigym[

For me, that does not compute. If one has spent a lifetime working and investing and saving to end up with $3 mil "in the bank." that is NOT "earning ZERO." I am not sure where the 13 years enters the equation.

tuttigym

link to original post

$3 million �in the bank� times zero equals zero in earnings over that period

link to original post

So who does that anyway?

tuttigym

Quote: tuttigymQuote: Ace2Interest rates on savings have been essentially zero since 2009.

$3 million �in the bank� times zero equals zero in earnings over that period

link to original post

So who does that anyway?

tuttigym

link to original post

The only way someone should have $3mm sitting in an almost-zero interest bank account is if they have like $50mm parked somewhere else.

Those are pretty strong words, especially coming from someone who required a second explanation of how to calculate 0% interest�$3 million times zero �did not compute� for you.Quote: tuttigymQuote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

Comprehension and reading skills are bailing on you Ace. That $6800 INCLUDES medical/health, auto, and homeowners. My property taxes were just $1200 this year too. I know you can do better. Just try a little harder.

tuttigym

link to original post

I understood what $6800 meant/included the first time you stated it�I don�t need things to be repeated. Your original post clearly states what�s included which makes me wonder if you even comprehend your own post.

That�s standard planning. When people forecast retirement with savings of $x and a withdrawal rate of x% (like 3 or 4%) they are counting on earning about that % in interestQuote: tuttigymQuote: Ace2Interest rates on savings have been essentially zero since 2009.Quote: tuttigym[

For me, that does not compute. If one has spent a lifetime working and investing and saving to end up with $3 mil "in the bank." that is NOT "earning ZERO." I am not sure where the 13 years enters the equation.

tuttigym

link to original post

$3 million �in the bank� times zero equals zero in earnings over that period

link to original post

So who does that anyway?

tuttigym

link to original post

If you withdraw 4% from an account that earns zero (or close to zero), your withdrawals decrease by 4% per year

Remember, the real interest rate on savings is �typically� around zero. Like you�re getting 5% which is 3.5% after taxes, minus 3.5% inflation. Part of what the Fed is doing now is bringing real interest rates up to zero. They�ve been negative for over a decade. In the last year, with higher inflation, they are very negative

Quote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

I thought he said that $6800 was all of his insurance (home, health, auto). my homeowners insurance alone is $8300 a year and that does not include flood insurance.

Quote: TigerWuQuote: tuttigymQuote: Ace2Interest rates on savings have been essentially zero since 2009.

$3 million �in the bank� times zero equals zero in earnings over that period

link to original post

So who does that anyway?

tuttigym

link to original post

The only way someone should have $3mm sitting in an almost-zero interest bank account is if they have like $50mm parked somewhere else.

link to original post

Not true. Many older people have all their money in the bank, earning nothing. I tried for years to get my mother to let me invest at least some, but she was afraid of losing any of it, so it sat at less than 1%interest. It's not at all uncommon.

If you had three million in a savings account ten years ago, you still have the money but are poorer. Today's dollar will only buy about 3/4s of what it did a decade ago.

Quote: Ace2[�I doubt I�ve spent $24k in medical expenses in my entire life

I have had 25 operations and my last one alone was close to $50k and that was just to remove a few gallstones. As far as I know my most expensive was my back surgery at $330k and that was just one night in the hospital.

Is this all due to conditions you were born with?Quote: DRichQuote: Ace2[�I doubt I�ve spent $24k in medical expenses in my entire life

I have had 25 operations and my last one alone was close to $50k and that was just to remove a few gallstones. As far as I know my most expensive was my back surgery at $330k and that was just one night in the hospital .

link to original post

Quote: Ace2Is this all due to conditions you were born with?Quote: DRichQuote: Ace2[�I doubt I�ve spent $24k in medical expenses in my entire life

I have had 25 operations and my last one alone was close to $50k and that was just to remove a few gallstones. As far as I know my most expensive was my back surgery at $330k and that was just one night in the hospital .

link to original post

link to original post

No, most of it was trauma.

Quote: billryanQuote: TigerWuQuote: tuttigymQuote: Ace2Interest rates on savings have been essentially zero since 2009.

$3 million �in the bank� times zero equals zero in earnings over that period

link to original post

So who does that anyway?

tuttigym

link to original post

The only way someone should have $3mm sitting in an almost-zero interest bank account is if they have like $50mm parked somewhere else.

link to original post

Not true. Many older people have all their money in the bank, earning nothing. I tried for years to get my mother to let me invest at least some, but she was afraid of losing any of it, so it sat at less than 1%interest. It's not at all uncommon.

If you had three million in a savings account ten years ago, you still have the money but are poorer. Today's dollar will only buy about 3/4s of what it did a decade ago.

link to original post

That's why I said should.

About ten years ago, I passed that advice on to my Godson, and he laughed. His accountant had told him pretty much the same thing only he said it about the first million. Inflation, I guess.

Quote: billryanThe advice I got many years ago was to forget about your first $100,000. Invest it and forget it exists. Never touch it, and in thirty years when you go to retire it will have blossomed into a tree you can prune as needed.

About ten years ago, I passed that advice on to my Godson, and he laughed. His accountant had told him pretty much the same thing only he said it about the first million. Inflation, I guess.

link to original post

LOL... if you actually have a first million you can just "forget about," then retirement won't be a problem at all because you're already rich.

Quote: DRichQuote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

I thought he said that $6800 was all of his insurance (home, health, auto). my homeowners insurance alone is $8300 a year and that does not include flood insurance.

link to original post

You should have bought a houseboat.

https://www.deepsailing.com/blog/cost-of-living-on-a-houseboat

Quote: rxwineQuote: DRichQuote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

I thought he said that $6800 was all of his insurance (home, health, auto). my homeowners insurance alone is $8300 a year and that does not include flood insurance.

link to original post

You should have bought a houseboat.

https://www.deepsailing.com/blog/cost-of-living-on-a-houseboat

link to original post

To get this back on topic. If I win the Powerball I may consider buying a houseboat.

Quote: DRichQuote: rxwineQuote: DRichQuote: Ace2$6,800 insurance? The only way I can imagine that number is if you have a home in a disaster-prone area (like Florida) that costs several thousand to insure

link to original post

I thought he said that $6800 was all of his insurance (home, health, auto). my homeowners insurance alone is $8300 a year and that does not include flood insurance.

link to original post

You should have bought a houseboat.

https://www.deepsailing.com/blog/cost-of-living-on-a-houseboat

link to original post

To get this back on topic. If I win the Powerball I may consider buying a houseboat.

link to original post

If I win Powerball, I'll consider buying you a houseboat, as well. I think I still owe you from Timbers.

Using my same formula, which I'll have to update after the jackpot hits, I project 2.4 winners the next drawing with a probability of at least one winner of 91%.

For the next drawing, I show a pre-tax ER of 80.1% and after paying 37% in taxes, 57.5%.

I found this amusing for some reason.

Of all my road trips, Death Valley was definitely the low point.

More money to be burnt Monday.

Quote: Mission146More money to be burnt Monday.

link to original post

I spent $4 for two tickets yesterday. I plan to do the same for Monday's drawing. With the understanding that I am essentially burning $4, I would say I will get >$4 worth of daydreaming value.

Quote: IndyJeffreyQuote: Mission146More money to be burnt Monday.

link to original post

I spent $4 for two tickets yesterday. I plan to do the same for Monday's drawing. With the understanding that I am essentially burning $4, I would say I will get >$4 worth of daydreaming value.

link to original post

I like to keep my daydreaming more in line with the value daydreaming has: nothing.