RoR in Bacc

I did just search up the risk of ruin calculator on the WoO site, but, that seems to require a player advantage - I don't believe there is one.

The angle here is to see how much of a bankroll you need, to successfully play through 5 shoes, with a minimal risk of total bankroll loss.

And, just for confirmation - I imagine the best bet on that No Comm Bacc with 6 paying 1 to 2 for a banker, is still, to bet the Banker - there's more possible winning combinations ? Or, does the 1 to 2 payout sufficiently affect the situation that flat betting player is a better option?

I have an idea that you can rearrange the usual formula slightly and come up with numbers like "If you start with 400 units, you will be 100% able to play 400 rounds, if you start with 300 units, you will be 87% likely to be able to play 400 rounds..." etc.

These are guesses. These numbers are wrong.

Quote: DieterI'm interested to see what the math experts do here.

I have an idea that you can rearrange the usual formula slightly and come up with numbers like "If you start with 400 units, you will be 100% able to play 400 rounds, if you start with 300 units, you will be 87% likely to be able to play 400 rounds..." etc.

These are guesses. These numbers are wrong.

link to original post

The RoR in a game with a house advantage is 100%.

I think this has been discussed before. As I recall, there is no easy way to approximate the answer of lasting x bets with a bankroll of y units. Simulations would need to be done.

That's simple. If there are an average of 400 hands in 5 shoes and you bet $100 per hand, then you need a bankroll of exactly 400 * $100 = $40,000 to "ensure" you could successfully play through 5 shoes. That way you can lose every single hand without busting your bankroll (not until the last hand).Quote: TwelveOr21If you flat bet Bacc, with the no commission variant, where 6 pays 1 to 2, assuming you bet the same 1 unit each and every time, how much of a bank roll would you need to ensure that you could successfully play through 5 shoes?

If you specify a confidence level like 90% then that's a different calculation

Uh!?Quote: WizardQuote: DieterI'm interested to see what the math experts do here.

I have an idea that you can rearrange the usual formula slightly and come up with numbers like "If you start with 400 units, you will be 100% able to play 400 rounds, if you start with 300 units, you will be 87% likely to be able to play 400 rounds..." etc.

These are guesses. These numbers are wrong.

link to original post

The RoR in a game with a house advantage is 100%.

I think this has been discussed before. As I recall, there is no easy way to approximate the answer of lasting x bets with a bankroll of y units. Simulations would need to be done.

link to original post

Wizard,

Please help me with that. is Risk of Ruin the probability of loss of entire bankroll?

If so, flat betting a fixed number of units into a low edge game will tend towards 100% as the number of units wagered approaches infinity. But surely it cannot be 100% for a small fixed number of wagers, E.g 400 wagers each of 1% of initial bankroll?

Quote: OnceDearWizard,

Please help me with that. is Risk of Ruin the probability of loss of entire bankroll?

If so, flat betting a fixed number of units into a low edge game will tend towards 100% as the number of units wagered approaches infinity. But surely it cannot be 100% for a small fixed number of wagers, E.g 400 wagers each of 1% of initial bankroll?

link to original post

There is confusion about what "risk of ruin" means and I'll take the blame for that.

Traditionally, risk of ruin means the probability of EVER going bankrupt with the alternative being a bankroll that grows infinitely. This can only be possible in a game with a positive expected value.

I think we should call the probability of going bust in a limited period of time by another term, to avoid confusion. Any suggestions for such a term?

For example, suppose the house edge is 0.41%, the player can take a 5% probability of trip ruin and wants to last 1,000 hands. That page says he would need a bankroll of 76 units.

I've been thinking of project ideas. Maybe I'll expand this to other games and/or try to find a general formula.

So losing 25 units in 100 hands, and 50 units in 400 hands, and 75 units in 800 hands is about a 3% RoR.

Oh that's right, I can't blame the machine, it's just trying to keep the total payback percentage above 99% and below 100%, and I'm screwing up its averages so bad with my win streaks, it goes extra hard with the losing streaks.

Quote: WizardThe RoR in a game with a house advantage is 100%.

I think this has been discussed before. As I recall, there is no easy way to approximate the answer of lasting x bets with a bankroll of y units. Simulations would need to be done.

link to original post

Hmm... we know expected loss for a given number of rounds, flat betting... yes?

And SD?

I trust your mathiness, but it seems to the casual observer that there might be something to go on.

Quote: WizardI knew I did something on this. My page on Risk of Ruin in blackjack states the bankroll size needed to last so-many hands in blackjack, given a specified probability of ruin.

For example, suppose the house edge is 0.41%, the player can take a 5% probability of trip ruin and wants to last 1,000 hands. That page says he would need a bankroll of 76 units.

I've been thinking of project ideas. Maybe I'll expand this to other games and/or try to find a general formula.

link to original post

Can I use this formula ?

Suppose you play n rounds of blackjack(normal distributed) and probability of loss more than B units is 5%, μ = - 0.0041, σ = 1.14

P(X <= -B) = 0.05

z = -1.645

(-B - n*μ) / (n^0.5 *σ) <= -1.645

B >= 63.4 units

There is a way to accurately estimate RoR for low edge games such as this one. After 400 hands, the expectation is to be down 5.83 units +/ 18.6. Since you are starting with a bankroll of 40 units, you would have to be 33.17 or more units below expectations to FINISH with a bankroll below 1 unit. The probability of finishing 33.17 / 18.6 deviations south of expectations is 3.73%. This probability does not consider your bankroll falling below zero DURING the session, but I've found that the RoR for low edge games is about double the chance of finishing the session in negative territory. This estimate would give an RoR of 3.73% * 2 = 7.46% (or 92.5% survival) which is fairly accurate

| Bankroll | Survive % | Bankroll | Survive % |

|---|---|---|---|

| 1 | 3.026 % | 26 | 75.197 % |

| 2 | 6.064 % | 27 | 77.165 % |

| 3 | 9.135 % | 28 | 79.033 % |

| 4 | 12.232 % | 29 | 80.796 % |

| 5 | 15.36 % | 30 | 82.449 % |

| 6 | 18.514 % | 31 | 83.995 % |

| 7 | 21.701 % | 32 | 85.438 % |

| 8 | 24.906 % | 33 | 86.784 % |

| 9 | 28.12 % | 34 | 88.04 % |

| 10 | 31.325 % | 35 | 89.2 % |

| 11 | 34.516 % | 36 | 90.27 % |

| 12 | 37.69 % | 37 | 91.262 % |

| 13 | 40.829 % | 38 | 92.166 % |

| 14 | 43.928 % | 39 | 92.994 % |

| 15 | 46.974 % | 40 | 93.753 % |

| 16 | 49.97 % | 41 | 94.444 % |

| 17 | 52.894 % | 42 | 95.069 % |

| 18 | 55.737 % | 43 | 95.637 % |

| 19 | 58.503 % | 44 | 96.149 % |

| 20 | 61.176 % | 45 | 96.609 % |

| 21 | 63.765 % | 46 | 97.021 % |

| 22 | 66.253 % | 47 | 97.39 % |

| 23 | 68.649 % | 48 | 97.719 % |

| 24 | 70.938 % | 49 | 98.013 % |

| 25 | 73.117 % | 50 | 98.273 % |

My estimation method described above gives an 86% chance of survival. Won't be quite as accurate since double zero roulette isn't exactly a low edge bet

Quote: ssho88Can I use this formula ?

Suppose you play n rounds of blackjack(normal distributed) and probability of loss more than B units is 5%, μ = - 0.0041, σ = 1.14

P(X <= -B) = 0.05

z = -1.645

(-B - n*μ) / (n^0.5 *σ) <= -1.645

B >= 63.4 units

link to original post

No. That assumes the player plays no matter what, including losing more than 63.4 units. We need something where if the player runs out of units, he is truly busted and can't play more on credit.

Quote: WizardQuote: ssho88Can I use this formula ?

Suppose you play n rounds of blackjack(normal distributed) and probability of loss more than B units is 5%, μ = - 0.0041, σ = 1.14

P(X <= -B) = 0.05

z = -1.645

(-B - n*μ) / (n^0.5 *σ) <= -1.645

B >= 63.4 units

link to original post

No. That assumes the player plays no matter what, including losing more than 63.4 units. We need something where if the player runs out of units, he is truly busted and can't play more on credit.

link to original post

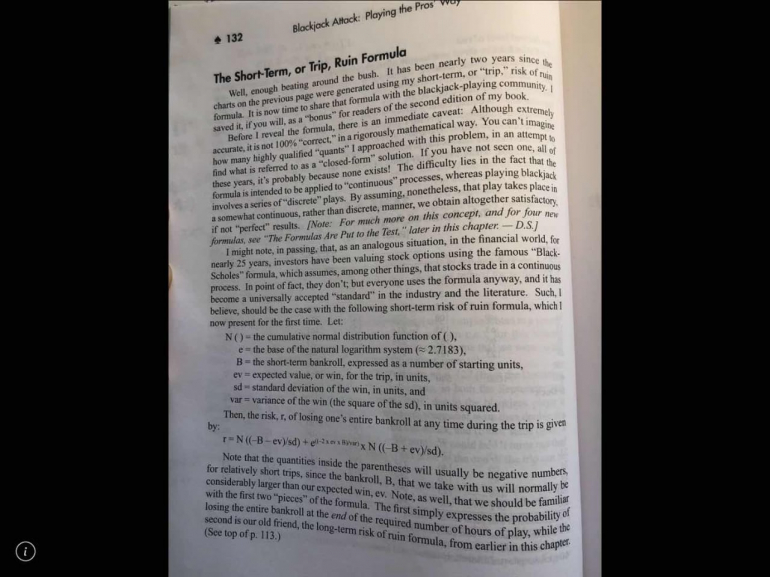

I think I can answer your question with below formula :-

An excerpt from BLACKJACK ATTACK(page 132)

I guess you have to do the reverse calculation to get the B value.

Now I'm wondering what the plot points for losing 25 unit sessions with a 3% RoR are all the way out to 50,000 hands. But I just lost another 25 units in 127 hands so I'm seriously losing worse than 3% RoR in the last 4 sessions.

If I'm down 550 units (22 sessions) in 21K hands, that'd be winning 10,225 hands and losing 10,775 hands, or winning $2,045,000 out of a total bet of $2,100,000 at a $100 table (win of -$55,000) which is a 97.38% payback rate (loss of $2.62/hand).

My real stats so far are 21,146 hands with a total bet of $2,417,865.00 and a total loss of $22,480 (-22.6 sessions), so on the bet amounts alone I'm getting a payback of 99.07%.

My average bet so far is $114.34 and I'm losing $1.06 per hand. My minimum bet is $30, but it's $120 if I'm at a $5,000 balance or more.

My ROKU 3 BJ game gives me $500 each day I log in, but the table limits move up with higher balances.

That formula uses the cumulative distribution twice so it's not really even a formula. More like the massaging of two statistical estimates.Quote: ssho88

I think I can answer your question with below formula :-

An excerpt from BLACKJACK ATTACK(page 132)

I guess you have to do the reverse calculation to get the B value.

link to original post

Note that this method also gives a RoR about double the probability of finishing the session with a busted bankroll. As I had mentioned above

Quote: ThatDonGuyHere's what I get after simulating 25 million sets of 5 8-deck shoes (full penetration, 1-11 card burn from the top):

Bankroll Survive % Bankroll Survive % 1 3.026 % 26 75.197 % 2 6.064 % 27 77.165 % 3 9.135 % 28 79.033 % 4 12.232 % 29 80.796 % 5 15.36 % 30 82.449 % 6 18.514 % 31 83.995 % 7 21.701 % 32 85.438 % 8 24.906 % 33 86.784 % 9 28.12 % 34 88.04 % 10 31.325 % 35 89.2 % 11 34.516 % 36 90.27 % 12 37.69 % 37 91.262 % 13 40.829 % 38 92.166 % 14 43.928 % 39 92.994 % 15 46.974 % 40 93.753 % 16 49.97 % 41 94.444 % 17 52.894 % 42 95.069 % 18 55.737 % 43 95.637 % 19 58.503 % 44 96.149 % 20 61.176 % 45 96.609 % 21 63.765 % 46 97.021 % 22 66.253 % 47 97.39 % 23 68.649 % 48 97.719 % 24 70.938 % 49 98.013 % 25 73.117 % 50 98.273 %

link to original post

Do you know if the numbers change dramatically if the number of shoes changes?

i.e. if the number of shoes was increased, is there a linear relationship between number of shoes and increased bankroll to maintain a really low RoR?

e.g. 50 is good for 5 shoes with a ~1.7% RoR.

Do we double it to 100 for 10 shoes for the same 1.7% RoR?

Quote: TwelveOr21

Do you know if the numbers change dramatically if the number of shoes changes?

i.e. if the number of shoes was increased, is there a linear relationship between number of shoes and increased bankroll to maintain a really low RoR?

e.g. 50 is good for 5 shoes with a ~1.7% RoR.

Do we double it to 100 for 10 shoes for the same 1.7% RoR?

link to original post

Here are the simulated (over 1 million sets of shoes each) results for RoRs (100% - success) for 6-25 shoes and bankrolls of 50-125:

| Bankroll | 6 shoes | 7 shoes | 8 shoes | 9 shoes | 10 shoes | 11 shoes | 12 shoes | 13 shoes | 14 shoes | 15 shoes |

|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 3.442 % | 5.428 % | 7.706 % | 10.145 % | 12.576 % | 15.131 % | 17.633 % | 20.136 % | 22.603 % | 24.939 % |

| 51 | 3.068 % | 4.917 % | 7.08 % | 9.4 % | 11.732 % | 14.219 % | 16.644 % | 19.092 % | 21.537 % | 23.852 % |

| 52 | 2.729 % | 4.444 % | 6.502 % | 8.704 % | 10.951 % | 13.35 % | 15.702 % | 18.084 % | 20.491 % | 22.763 % |

| 53 | 2.419 % | 3.994 % | 5.951 % | 8.041 % | 10.188 % | 12.517 % | 14.792 % | 17.137 % | 19.488 % | 21.723 % |

| 54 | 2.142 % | 3.595 % | 5.426 % | 7.409 % | 9.469 % | 11.721 % | 13.928 % | 16.222 % | 18.518 % | 20.726 % |

| 55 | 1.889 % | 3.238 % | 4.958 % | 6.83 % | 8.799 % | 10.972 % | 13.096 % | 15.335 % | 17.583 % | 19.768 % |

| 56 | 1.668 % | 2.908 % | 4.514 % | 6.29 % | 8.167 % | 10.259 % | 12.318 % | 14.497 % | 16.678 % | 18.813 % |

| 57 | 1.464 % | 2.603 % | 4.096 % | 5.777 % | 7.567 % | 9.57 % | 11.556 % | 13.668 % | 15.811 % | 17.895 % |

| 58 | 1.282 % | 2.327 % | 3.712 % | 5.299 % | 7.011 % | 8.929 % | 10.844 % | 12.892 % | 14.961 % | 17.02 % |

| 59 | 1.123 % | 2.075 % | 3.354 % | 4.843 % | 6.477 % | 8.321 % | 10.171 % | 12.129 % | 14.132 % | 16.161 % |

| 60 | 0.982 % | 1.845 % | 3.031 % | 4.449 % | 5.978 % | 7.734 % | 9.531 % | 11.414 % | 13.358 % | 15.336 % |

| 61 | 0.857 % | 1.642 % | 2.741 % | 4.071 % | 5.513 % | 7.192 % | 8.914 % | 10.724 % | 12.622 % | 14.556 % |

| 62 | 0.745 % | 1.462 % | 2.463 % | 3.715 % | 5.09 % | 6.677 % | 8.33 % | 10.07 % | 11.925 % | 13.801 % |

| 63 | 0.648 % | 1.298 % | 2.216 % | 3.375 % | 4.69 % | 6.186 % | 7.771 % | 9.439 % | 11.244 % | 13.083 % |

| 64 | 0.564 % | 1.147 % | 1.992 % | 3.075 % | 4.308 % | 5.722 % | 7.256 % | 8.851 % | 10.594 % | 12.377 % |

| 65 | 0.488 % | 1.013 % | 1.788 % | 2.794 % | 3.951 % | 5.304 % | 6.775 % | 8.296 % | 9.988 % | 11.696 % |

| 66 | 0.42 % | 0.9 % | 1.605 % | 2.525 % | 3.611 % | 4.898 % | 6.302 % | 7.76 % | 9.395 % | 11.059 % |

| 67 | 0.36 % | 0.794 % | 1.435 % | 2.29 % | 3.314 % | 4.528 % | 5.865 % | 7.255 % | 8.836 % | 10.453 % |

| 68 | 0.308 % | 0.703 % | 1.287 % | 2.079 % | 3.019 % | 4.183 % | 5.452 % | 6.778 % | 8.297 % | 9.861 % |

| 69 | 0.265 % | 0.618 % | 1.151 % | 1.876 % | 2.757 % | 3.856 % | 5.055 % | 6.332 % | 7.794 % | 9.287 % |

| 70 | 0.225 % | 0.541 % | 1.025 % | 1.693 % | 2.524 % | 3.546 % | 4.676 % | 5.904 % | 7.305 % | 8.746 % |

| 71 | 0.191 % | 0.477 % | 0.909 % | 1.523 % | 2.301 % | 3.259 % | 4.335 % | 5.494 % | 6.839 % | 8.216 % |

| 72 | 0.161 % | 0.413 % | 0.809 % | 1.367 % | 2.097 % | 2.989 % | 4.001 % | 5.112 % | 6.394 % | 7.724 % |

| 73 | 0.139 % | 0.36 % | 0.721 % | 1.228 % | 1.913 % | 2.742 % | 3.694 % | 4.756 % | 5.992 % | 7.248 % |

| 74 | 0.116 % | 0.316 % | 0.638 % | 1.105 % | 1.737 % | 2.513 % | 3.406 % | 4.427 % | 5.607 % | 6.803 % |

| 75 | 0.098 % | 0.277 % | 0.559 % | 0.993 % | 1.573 % | 2.3 % | 3.149 % | 4.102 % | 5.235 % | 6.375 % |

| 76 | 0.083 % | 0.238 % | 0.497 % | 0.894 % | 1.428 % | 2.101 % | 2.903 % | 3.811 % | 4.897 % | 5.972 % |

| 77 | 0.069 % | 0.204 % | 0.434 % | 0.799 % | 1.288 % | 1.925 % | 2.677 % | 3.532 % | 4.554 % | 5.593 % |

| 78 | 0.058 % | 0.177 % | 0.385 % | 0.713 % | 1.165 % | 1.756 % | 2.455 % | 3.267 % | 4.238 % | 5.247 % |

| 79 | 0.049 % | 0.152 % | 0.337 % | 0.637 % | 1.042 % | 1.6 % | 2.261 % | 3.022 % | 3.935 % | 4.906 % |

| 80 | 0.042 % | 0.131 % | 0.298 % | 0.563 % | 0.934 % | 1.455 % | 2.072 % | 2.793 % | 3.659 % | 4.588 % |

| 81 | 0.035 % | 0.112 % | 0.265 % | 0.499 % | 0.838 % | 1.32 % | 1.908 % | 2.571 % | 3.393 % | 4.277 % |

| 82 | 0.029 % | 0.096 % | 0.23 % | 0.441 % | 0.758 % | 1.192 % | 1.742 % | 2.366 % | 3.15 % | 3.986 % |

| 83 | 0.025 % | 0.082 % | 0.202 % | 0.39 % | 0.678 % | 1.081 % | 1.598 % | 2.184 % | 2.923 % | 3.719 % |

| 84 | 0.02 % | 0.07 % | 0.176 % | 0.348 % | 0.609 % | 0.986 % | 1.459 % | 2.007 % | 2.707 % | 3.468 % |

| 85 | 0.017 % | 0.06 % | 0.152 % | 0.309 % | 0.545 % | 0.894 % | 1.335 % | 1.846 % | 2.509 % | 3.232 % |

| 86 | 0.014 % | 0.05 % | 0.133 % | 0.269 % | 0.484 % | 0.81 % | 1.219 % | 1.696 % | 2.323 % | 3.014 % |

| 87 | 0.011 % | 0.042 % | 0.116 % | 0.237 % | 0.432 % | 0.736 % | 1.113 % | 1.56 % | 2.15 % | 2.804 % |

| 88 | 0.009 % | 0.035 % | 0.1 % | 0.207 % | 0.383 % | 0.666 % | 1.01 % | 1.435 % | 1.978 % | 2.602 % |

| 89 | 0.008 % | 0.028 % | 0.086 % | 0.183 % | 0.341 % | 0.602 % | 0.922 % | 1.315 % | 1.823 % | 2.418 % |

| 90 | 0.007 % | 0.024 % | 0.074 % | 0.158 % | 0.3 % | 0.541 % | 0.838 % | 1.206 % | 1.68 % | 2.234 % |

| 91 | 0.005 % | 0.019 % | 0.065 % | 0.139 % | 0.267 % | 0.484 % | 0.762 % | 1.106 % | 1.544 % | 2.066 % |

| 92 | 0.004 % | 0.016 % | 0.056 % | 0.119 % | 0.238 % | 0.435 % | 0.691 % | 1.013 % | 1.423 % | 1.917 % |

| 93 | 0.003 % | 0.014 % | 0.047 % | 0.105 % | 0.208 % | 0.389 % | 0.625 % | 0.923 % | 1.303 % | 1.765 % |

| 94 | 0.003 % | 0.012 % | 0.04 % | 0.09 % | 0.181 % | 0.348 % | 0.561 % | 0.844 % | 1.194 % | 1.63 % |

| 95 | 0.002 % | 0.01 % | 0.034 % | 0.077 % | 0.159 % | 0.313 % | 0.505 % | 0.768 % | 1.097 % | 1.514 % |

| 96 | 0.002 % | 0.008 % | 0.029 % | 0.067 % | 0.139 % | 0.276 % | 0.456 % | 0.699 % | 1.007 % | 1.394 % |

| 97 | 0.001 % | 0.007 % | 0.025 % | 0.057 % | 0.122 % | 0.249 % | 0.41 % | 0.636 % | 0.919 % | 1.286 % |

| 98 | 0.001 % | 0.006 % | 0.023 % | 0.05 % | 0.106 % | 0.224 % | 0.367 % | 0.578 % | 0.845 % | 1.183 % |

| 99 | 0.001 % | 0.004 % | 0.019 % | 0.043 % | 0.093 % | 0.199 % | 0.329 % | 0.528 % | 0.77 % | 1.088 % |

| 100 | 0 % | 0.003 % | 0.015 % | 0.037 % | 0.08 % | 0.176 % | 0.294 % | 0.476 % | 0.702 % | 0.997 % |

| 101 | 0 % | 0.003 % | 0.012 % | 0.032 % | 0.07 % | 0.158 % | 0.264 % | 0.428 % | 0.641 % | 0.912 % |

| 102 | 0 % | 0.002 % | 0.011 % | 0.027 % | 0.061 % | 0.141 % | 0.234 % | 0.386 % | 0.587 % | 0.838 % |

| 103 | 0 % | 0.002 % | 0.01 % | 0.023 % | 0.055 % | 0.125 % | 0.208 % | 0.349 % | 0.535 % | 0.766 % |

| 104 | 0 % | 0.002 % | 0.008 % | 0.02 % | 0.049 % | 0.112 % | 0.187 % | 0.319 % | 0.488 % | 0.703 % |

| 105 | 0 % | 0.002 % | 0.007 % | 0.017 % | 0.044 % | 0.099 % | 0.165 % | 0.289 % | 0.448 % | 0.641 % |

| 106 | 0 % | 0.001 % | 0.006 % | 0.015 % | 0.038 % | 0.087 % | 0.148 % | 0.258 % | 0.406 % | 0.588 % |

| 107 | 0 % | 0.001 % | 0.005 % | 0.013 % | 0.032 % | 0.076 % | 0.132 % | 0.229 % | 0.363 % | 0.541 % |

| 108 | 0 % | 0.001 % | 0.004 % | 0.011 % | 0.029 % | 0.064 % | 0.117 % | 0.204 % | 0.327 % | 0.495 % |

| 109 | 0 % | 0.001 % | 0.003 % | 0.009 % | 0.026 % | 0.055 % | 0.104 % | 0.183 % | 0.297 % | 0.452 % |

| 110 | 0 % | 0.001 % | 0.003 % | 0.008 % | 0.022 % | 0.049 % | 0.091 % | 0.164 % | 0.268 % | 0.41 % |

| 111 | 0 % | 0 % | 0.003 % | 0.007 % | 0.02 % | 0.043 % | 0.08 % | 0.147 % | 0.243 % | 0.376 % |

| 112 | 0 % | 0 % | 0.003 % | 0.005 % | 0.016 % | 0.039 % | 0.072 % | 0.131 % | 0.222 % | 0.342 % |

| 113 | 0 % | 0 % | 0.002 % | 0.005 % | 0.013 % | 0.034 % | 0.063 % | 0.117 % | 0.198 % | 0.31 % |

| 114 | 0 % | 0 % | 0.002 % | 0.004 % | 0.011 % | 0.03 % | 0.055 % | 0.105 % | 0.178 % | 0.286 % |

| 115 | 0 % | 0 % | 0.002 % | 0.003 % | 0.009 % | 0.027 % | 0.048 % | 0.094 % | 0.16 % | 0.258 % |

| 116 | 0 % | 0 % | 0.001 % | 0.003 % | 0.007 % | 0.023 % | 0.042 % | 0.084 % | 0.143 % | 0.234 % |

| 117 | 0 % | 0 % | 0.001 % | 0.003 % | 0.006 % | 0.021 % | 0.038 % | 0.075 % | 0.13 % | 0.212 % |

| 118 | 0 % | 0 % | 0.001 % | 0.002 % | 0.005 % | 0.018 % | 0.033 % | 0.068 % | 0.116 % | 0.191 % |

| 119 | 0 % | 0 % | 0.001 % | 0.002 % | 0.004 % | 0.015 % | 0.029 % | 0.061 % | 0.106 % | 0.173 % |

| 120 | 0 % | 0 % | 0.001 % | 0.002 % | 0.003 % | 0.014 % | 0.027 % | 0.054 % | 0.095 % | 0.155 % |

| 121 | 0 % | 0 % | 0.001 % | 0.001 % | 0.003 % | 0.011 % | 0.025 % | 0.048 % | 0.086 % | 0.139 % |

| 122 | 0 % | 0 % | 0.001 % | 0.001 % | 0.003 % | 0.01 % | 0.023 % | 0.043 % | 0.077 % | 0.126 % |

| 123 | 0 % | 0 % | 0 % | 0.001 % | 0.002 % | 0.009 % | 0.019 % | 0.039 % | 0.069 % | 0.115 % |

| 124 | 0 % | 0 % | 0 % | 0.001 % | 0.002 % | 0.008 % | 0.017 % | 0.035 % | 0.061 % | 0.105 % |

| 125 | 0 % | 0 % | 0 % | 0 % | 0.001 % | 0.007 % | 0.015 % | 0.031 % | 0.054 % | 0.094 % |

| Bankroll | 16 shoes | 17 shoes | 18 shoes | 19 shoes | 20 shoes | 21 shoes | 22 shoes | 23 shoes | 24 shoes |

|---|---|---|---|---|---|---|---|---|---|

| 50 | 27.221 % | 29.406 % | 31.565 % | 33.536 % | 35.48 % | 37.409 % | 39.102 % | 40.922 % | 42.603 % |

| 51 | 26.09 % | 28.258 % | 30.405 % | 32.388 % | 34.33 % | 36.236 % | 37.937 % | 39.777 % | 41.436 % |

| 52 | 24.986 % | 27.141 % | 29.28 % | 31.261 % | 33.166 % | 35.098 % | 36.776 % | 38.64 % | 40.303 % |

| 53 | 23.912 % | 26.031 % | 28.169 % | 30.155 % | 32.041 % | 33.977 % | 35.646 % | 37.493 % | 39.2 % |

| 54 | 22.893 % | 24.972 % | 27.081 % | 29.058 % | 30.932 % | 32.873 % | 34.531 % | 36.378 % | 38.104 % |

| 55 | 21.865 % | 23.935 % | 26.024 % | 28.008 % | 29.847 % | 31.779 % | 33.445 % | 35.285 % | 37.022 % |

| 56 | 20.891 % | 22.927 % | 24.986 % | 26.959 % | 28.794 % | 30.709 % | 32.363 % | 34.208 % | 35.937 % |

| 57 | 19.955 % | 21.939 % | 23.979 % | 25.927 % | 27.749 % | 29.678 % | 31.314 % | 33.173 % | 34.853 % |

| 58 | 19.02 % | 20.983 % | 22.981 % | 24.936 % | 26.73 % | 28.654 % | 30.274 % | 32.144 % | 33.818 % |

| 59 | 18.139 % | 20.054 % | 22.021 % | 23.98 % | 25.736 % | 27.641 % | 29.259 % | 31.123 % | 32.79 % |

| 60 | 17.262 % | 19.167 % | 21.081 % | 23.038 % | 24.79 % | 26.664 % | 28.277 % | 30.115 % | 31.777 % |

| 61 | 16.438 % | 18.307 % | 20.175 % | 22.116 % | 23.845 % | 25.71 % | 27.303 % | 29.128 % | 30.772 % |

| 62 | 15.641 % | 17.457 % | 19.307 % | 21.232 % | 22.92 % | 24.764 % | 26.356 % | 28.162 % | 29.798 % |

| 63 | 14.869 % | 16.643 % | 18.465 % | 20.358 % | 22.033 % | 23.839 % | 25.42 % | 27.216 % | 28.846 % |

| 64 | 14.114 % | 15.851 % | 17.651 % | 19.508 % | 21.17 % | 22.929 % | 24.518 % | 26.294 % | 27.899 % |

| 65 | 13.393 % | 15.093 % | 16.872 % | 18.682 % | 20.322 % | 22.062 % | 23.636 % | 25.387 % | 26.972 % |

| 66 | 12.706 % | 14.359 % | 16.085 % | 17.873 % | 19.488 % | 21.212 % | 22.771 % | 24.496 % | 26.063 % |

| 67 | 12.055 % | 13.651 % | 15.347 % | 17.095 % | 18.693 % | 20.375 % | 21.922 % | 23.615 % | 25.171 % |

| 68 | 11.423 % | 12.983 % | 14.622 % | 16.344 % | 17.898 % | 19.551 % | 21.081 % | 22.748 % | 24.3 % |

| 69 | 10.798 % | 12.329 % | 13.941 % | 15.607 % | 17.134 % | 18.774 % | 20.268 % | 21.933 % | 23.46 % |

| 70 | 10.2 % | 11.692 % | 13.267 % | 14.904 % | 16.397 % | 18.002 % | 19.482 % | 21.122 % | 22.636 % |

| 71 | 9.634 % | 11.091 % | 12.615 % | 14.222 % | 15.694 % | 17.27 % | 18.713 % | 20.319 % | 21.806 % |

| 72 | 9.091 % | 10.513 % | 11.995 % | 13.566 % | 14.992 % | 16.529 % | 17.961 % | 19.537 % | 21.006 % |

| 73 | 8.582 % | 9.963 % | 11.405 % | 12.93 % | 14.316 % | 15.818 % | 17.238 % | 18.788 % | 20.244 % |

| 74 | 8.097 % | 9.439 % | 10.839 % | 12.302 % | 13.668 % | 15.134 % | 16.532 % | 18.062 % | 19.49 % |

| 75 | 7.636 % | 8.921 % | 10.296 % | 11.712 % | 13.05 % | 14.48 % | 15.837 % | 17.35 % | 18.759 % |

| 76 | 7.194 % | 8.412 % | 9.772 % | 11.128 % | 12.457 % | 13.853 % | 15.18 % | 16.651 % | 18.048 % |

| 77 | 6.768 % | 7.941 % | 9.243 % | 10.571 % | 11.882 % | 13.239 % | 14.552 % | 15.972 % | 17.35 % |

| 78 | 6.364 % | 7.502 % | 8.76 % | 10.032 % | 11.307 % | 12.649 % | 13.951 % | 15.311 % | 16.677 % |

| 79 | 5.977 % | 7.081 % | 8.303 % | 9.527 % | 10.765 % | 12.073 % | 13.349 % | 14.671 % | 16.003 % |

| 80 | 5.613 % | 6.673 % | 7.849 % | 9.045 % | 10.246 % | 11.521 % | 12.771 % | 14.041 % | 15.363 % |

| 81 | 5.261 % | 6.281 % | 7.418 % | 8.572 % | 9.735 % | 10.994 % | 12.203 % | 13.448 % | 14.746 % |

| 82 | 4.925 % | 5.92 % | 7.019 % | 8.131 % | 9.245 % | 10.475 % | 11.663 % | 12.87 % | 14.133 % |

| 83 | 4.607 % | 5.56 % | 6.634 % | 7.705 % | 8.776 % | 9.971 % | 11.125 % | 12.307 % | 13.561 % |

| 84 | 4.309 % | 5.23 % | 6.257 % | 7.297 % | 8.322 % | 9.486 % | 10.611 % | 11.767 % | 13.005 % |

| 85 | 4.029 % | 4.908 % | 5.898 % | 6.908 % | 7.889 % | 9.014 % | 10.122 % | 11.241 % | 12.467 % |

| 86 | 3.777 % | 4.605 % | 5.552 % | 6.525 % | 7.474 % | 8.57 % | 9.656 % | 10.741 % | 11.942 % |

| 87 | 3.525 % | 4.332 % | 5.223 % | 6.159 % | 7.076 % | 8.14 % | 9.2 % | 10.25 % | 11.44 % |

| 88 | 3.29 % | 4.063 % | 4.913 % | 5.821 % | 6.71 % | 7.723 % | 8.759 % | 9.781 % | 10.948 % |

| 89 | 3.065 % | 3.799 % | 4.61 % | 5.49 % | 6.357 % | 7.319 % | 8.339 % | 9.338 % | 10.45 % |

| 90 | 2.855 % | 3.559 % | 4.339 % | 5.183 % | 6.017 % | 6.943 % | 7.93 % | 8.912 % | 9.988 % |

| 91 | 2.658 % | 3.325 % | 4.079 % | 4.877 % | 5.685 % | 6.573 % | 7.544 % | 8.502 % | 9.544 % |

| 92 | 2.472 % | 3.102 % | 3.825 % | 4.594 % | 5.364 % | 6.228 % | 7.166 % | 8.104 % | 9.1 % |

| 93 | 2.293 % | 2.899 % | 3.589 % | 4.329 % | 5.063 % | 5.901 % | 6.803 % | 7.715 % | 8.676 % |

| 94 | 2.132 % | 2.706 % | 3.362 % | 4.08 % | 4.779 % | 5.595 % | 6.45 % | 7.345 % | 8.277 % |

| 95 | 1.977 % | 2.53 % | 3.148 % | 3.839 % | 4.518 % | 5.299 % | 6.118 % | 6.982 % | 7.889 % |

| 96 | 1.835 % | 2.356 % | 2.951 % | 3.601 % | 4.263 % | 5.013 % | 5.796 % | 6.633 % | 7.525 % |

| 97 | 1.696 % | 2.197 % | 2.761 % | 3.388 % | 4.015 % | 4.738 % | 5.492 % | 6.301 % | 7.169 % |

| 98 | 1.566 % | 2.044 % | 2.586 % | 3.18 % | 3.784 % | 4.483 % | 5.209 % | 5.981 % | 6.817 % |

| 99 | 1.448 % | 1.897 % | 2.42 % | 2.981 % | 3.569 % | 4.227 % | 4.924 % | 5.672 % | 6.49 % |

| 100 | 1.337 % | 1.762 % | 2.258 % | 2.795 % | 3.352 % | 3.984 % | 4.66 % | 5.373 % | 6.17 % |

| 101 | 1.237 % | 1.639 % | 2.107 % | 2.619 % | 3.151 % | 3.745 % | 4.41 % | 5.092 % | 5.856 % |

| 102 | 1.141 % | 1.522 % | 1.969 % | 2.445 % | 2.957 % | 3.524 % | 4.166 % | 4.821 % | 5.555 % |

| 103 | 1.048 % | 1.414 % | 1.835 % | 2.288 % | 2.775 % | 3.319 % | 3.929 % | 4.571 % | 5.278 % |

| 104 | 0.97 % | 1.314 % | 1.71 % | 2.136 % | 2.6 % | 3.123 % | 3.706 % | 4.323 % | 5.011 % |

| 105 | 0.897 % | 1.216 % | 1.59 % | 1.996 % | 2.44 % | 2.94 % | 3.507 % | 4.092 % | 4.756 % |

| 106 | 0.827 % | 1.12 % | 1.477 % | 1.86 % | 2.282 % | 2.76 % | 3.307 % | 3.868 % | 4.514 % |

| 107 | 0.758 % | 1.034 % | 1.372 % | 1.729 % | 2.135 % | 2.586 % | 3.12 % | 3.652 % | 4.28 % |

| 108 | 0.693 % | 0.952 % | 1.271 % | 1.612 % | 2 % | 2.423 % | 2.939 % | 3.451 % | 4.052 % |

| 109 | 0.636 % | 0.877 % | 1.173 % | 1.505 % | 1.867 % | 2.275 % | 2.759 % | 3.254 % | 3.83 % |

| 110 | 0.585 % | 0.809 % | 1.082 % | 1.396 % | 1.749 % | 2.134 % | 2.593 % | 3.065 % | 3.63 % |

| 111 | 0.535 % | 0.747 % | 1.008 % | 1.299 % | 1.633 % | 2.001 % | 2.439 % | 2.89 % | 3.434 % |

| 112 | 0.49 % | 0.689 % | 0.936 % | 1.208 % | 1.521 % | 1.878 % | 2.298 % | 2.73 % | 3.245 % |

| 113 | 0.452 % | 0.631 % | 0.863 % | 1.125 % | 1.418 % | 1.756 % | 2.161 % | 2.577 % | 3.063 % |

| 114 | 0.411 % | 0.581 % | 0.799 % | 1.042 % | 1.322 % | 1.645 % | 2.023 % | 2.429 % | 2.897 % |

| 115 | 0.377 % | 0.534 % | 0.738 % | 0.968 % | 1.227 % | 1.539 % | 1.897 % | 2.285 % | 2.728 % |

| 116 | 0.346 % | 0.491 % | 0.683 % | 0.898 % | 1.144 % | 1.439 % | 1.774 % | 2.15 % | 2.57 % |

| 117 | 0.317 % | 0.45 % | 0.633 % | 0.828 % | 1.067 % | 1.343 % | 1.663 % | 2.026 % | 2.419 % |

| 118 | 0.288 % | 0.418 % | 0.581 % | 0.764 % | 0.997 % | 1.256 % | 1.559 % | 1.902 % | 2.275 % |

| 119 | 0.262 % | 0.383 % | 0.539 % | 0.707 % | 0.926 % | 1.164 % | 1.461 % | 1.793 % | 2.137 % |

| 120 | 0.24 % | 0.353 % | 0.498 % | 0.654 % | 0.856 % | 1.081 % | 1.363 % | 1.688 % | 2.004 % |

| 121 | 0.218 % | 0.321 % | 0.459 % | 0.602 % | 0.797 % | 1.008 % | 1.272 % | 1.584 % | 1.887 % |

| 122 | 0.197 % | 0.292 % | 0.424 % | 0.553 % | 0.738 % | 0.939 % | 1.188 % | 1.487 % | 1.777 % |

| 123 | 0.177 % | 0.266 % | 0.39 % | 0.505 % | 0.679 % | 0.876 % | 1.11 % | 1.394 % | 1.666 % |

| 124 | 0.163 % | 0.243 % | 0.357 % | 0.466 % | 0.629 % | 0.815 % | 1.043 % | 1.308 % | 1.561 % |

| 125 | 0.149 % | 0.221 % | 0.327 % | 0.43 % | 0.584 % | 0.758 % | 0.973 % | 1.225 % | 1.466 % |